Following the Money: Trends in Bitcoin Venture Capital Investment

CoinDesk is releasing its 'State of Bitcoin 2014' report on Tuesday, which takes an in-depth look into the evolution of bitcoin and the potential hurdles it is still yet to face.

This article is the first of a two-part series drawn from the report. The series looks at the trends in venture capital investment in bitcoin.

It assesses how venture investment in bitcoin to date compares with other related investment sectors (eg financial technology), or previous major waves of investment (eg the Internet).

It also examines the types of Bitcoin companies venture investors have focused their funding on.

Look out for part two, which will be published tomorrow and focuses on which regions have been receiving the lion's share of venture investment in bitcoin.

Venture investment: early Internet vs early bitcoin

Venture capitalist and Internet pioneer Marc Andreessen recently compared the current understanding of bitcoin's overall potential, as well as its current stage of development, to the Internet circa 1993 and the PC in 1975.

Does the level of venture capital invested in bitcoin to date reflect Andreessen's assessment?

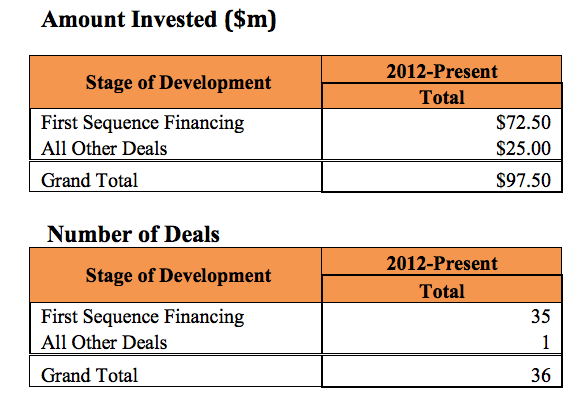

Table 1: VC Investments in Bitcoin Companies, 2012-Present

Sources: CoinDesk, Dow Jones VentureSource, VentureScanner

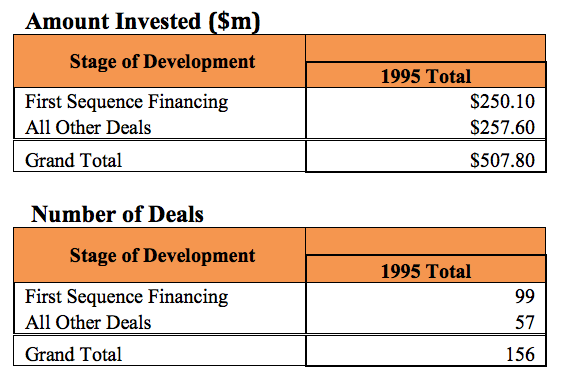

Comparing this bitcoin investment to date with investment in the early Internet, (Table 2) reveals that that significantly less funding (approximately 20%) has been allocated to Bitcoin compared to Internet startups, which pulled in just over $500m in venture investment in 1995.

Table 2: VC Investments in US Internet Companies, 1995

Sources: PricewaterhouseCoopers, National Venture Capital Association

With regards to the above comparison, there are several important caveats. First, due to data availability limitations there is no way to compare the Internet investments circa 1993 with bitcoin 2014, as 1995 is the earliest year in which we have Internet investment data.[1]

The above Internet investment data also reflect only US investments as global data are not available. While the vast majority of early Internet investment was US-based the $507m figure likely understates total global Internet investment in 1995.

On the Bitcoin side, the $97.5m in venture capital that has been publicly reported underestimates the total, which would include unreported venture investment, by tens of millions of dollars.

For example, we know that Andreessen Horowitz has invested just under $50m in bitcoin-related startups, and that Coinbase and Ripple have only received $25m and $9 million, respectively, in rounds which Andreessen Horowitz may have participated. CoinDesk is also aware of, but not privy to disclose, other million-dollar-plus funding rounds in Bitcoin startups, and these figures are, therefore, excluded from this analysis.

Also, it has been estimated that upwards of $200m has been invested in bitcoin mining hardware and infrastructure to date, a figure which exceeds even a less conservative estimate of the total venture capital invested in bitcoin to date. Perhaps the appropriate Internet analogy to this mining hardware investment is to compare it to the significant fiber optic and broadband infrastructure investments that was occurring alongside the investment in Internet startups.

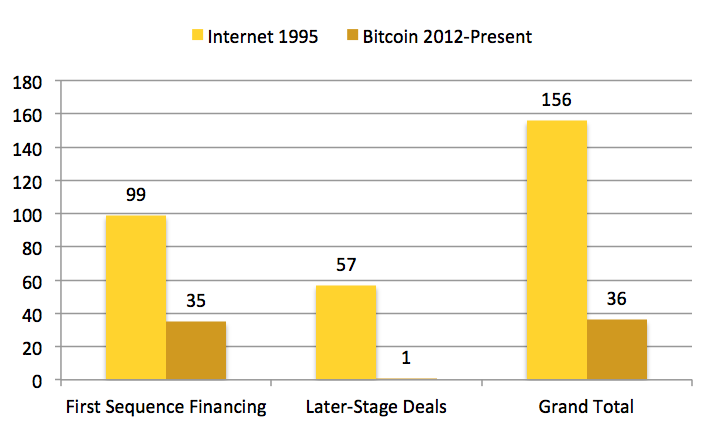

Chart 1: Number of VC-backed Companies: early Internet vs early bitcoin

Sources: PricewaterhouseCoopers, National Venture Capital Association, CoinDesk, Dow Jones VentureSource, VentureScanner

Looking at the number of deals from 1995, we can see a total of 156 total funding rounds, with nearly two-thirds of the rounds being first sequence financings.

In contrast, all but one Bitcoin startup financing round (Coinbase's November 2013 $25m Series B) have been first or seed round investments.

In short, the data fit Andreessen's story that the current Bitcoin investment lifecycle is relatively less mature than the Internet's circa 1995, and perhaps more akin to where the Internet investment environment stood in 1993.

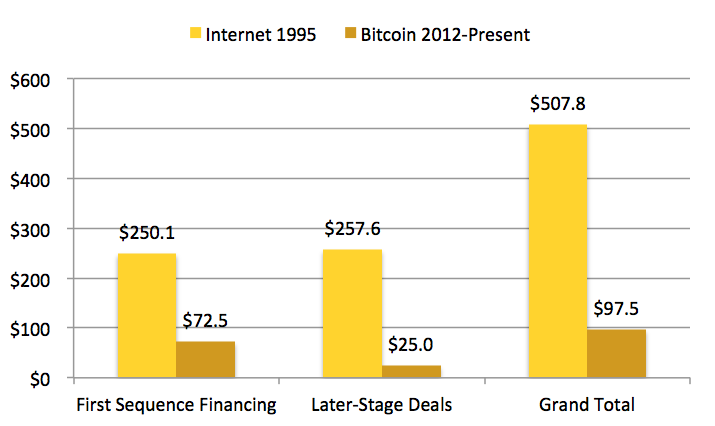

Chart 2: VC Investment in 1995 Internet Companies vs bitcoin

Sources: PricewaterhouseCoopers, National Venture Capital Association, CoinDesk, Dow Jones VentureSource, VentureScanner

Looking at the data on VC investments in Internet companies for 1995, we can also see that a much greater sum of funding was directed towards Internet companies than has been directed at Bitcoin startups to date (Chart 2).

In 1995 there was $508m invested in Internet companies, an amount which was just about evenly split between first sequence and later stage financings. Over 50% of Internet startup funding was going to just one-third of the venture-backed Internet companies.

According to the National Venture Capital Association there was $7.2 billion invested in Internet companies based in the U.S. from 1995-2013. If VCs are proven correct that Bitcoin represents an opportunity on par with the Internet then we can expect investment in Bitcoin startups to increase by an order of magnitude or more from current levels.

30 VC-backed bitcoin startups across five distinct sectors

There have been 30 bitcoin companies in total that have received publicly-reported venture funding to date (see Table 3).

| Company | Classification |

|---|---|

| BTC China (Shanghai Satuxi Network) | Exchange |

| HKCex | Exchange |

| itBit | Exchange |

| Korbit | Exchange |

| Coinfloor | Exchange |

| Coinsetter | Exchange |

| TradeHill | Exchange |

| Vaurum | Exchange |

| BTC.sx | Exchange |

| COINFIRMA | Financial Services |

| Digital Currencies FinTech | Financial Services |

| GogoCoin | Financial Services |

| Ripple Labs | Financial Services |

| BitAccess | Financial Services |

| Bex.io / Spawngrid | Financial Services |

| Buttercoin | Financial Services |

| BitFury | Mining Hardware |

| Avalon Clones | Mining Hardware |

| 21E6 | Mining Hardware |

| GoCoin | Payment Processor |

| Bitinstant | Payment Processor |

| BitPay | Payment Processor |

| Coinbase | Payment Processor/Wallet |

| Safello | Payment Processor/Wallet |

| Coinplug | Payment Processor/Wallet |

| CoinJar Pty | Wallet |

| Armory Technologies | Wallet |

| Gliph | Wallet |

| Beijing Lekuda Network Technology | Unknown |

| Circle Internet Financial | Unknown |

Sources: CoinDesk, DowJones VentureSource, VentureScanner

Note: A number of additional companies not included in the table are rumoured to have received non-publicly disclosed venture capital investment.

The universe of venture-backed Bitcoin companies can be broadly classified into the following five distinct sectors:

- Exchanges – companies that operate a bitcoin trading platform (eg BTC China)

- Financial Services – the broadest category, including everything from bitcoin ATM operators (eg BitAccess) to white label exchange providers (eg Buttercoin) to alternative payment networks (eg Ripple) to bitcoin gift cards (eg GogoCoin)

- Mining Hardware – producers of bitcoin mining equipment like ASICs (eg BitFury)

- Payment Processors – outsourced virtual alternative currency payment solutions (eg BitPay)

- Wallets – secure storage and transfer mechanisms for digital alternative currency. Several payment processors also have wallets (eg Gliph)

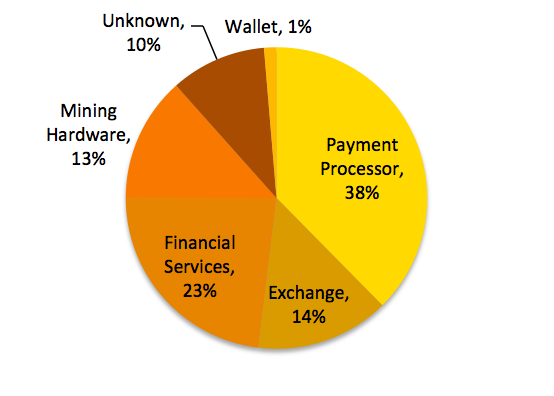

Chart 3: Sector distribution of Bitcoin VC investment

Sector-distribution-Bitcoin-VC-investment

Payment Processors lead the way in terms of total share of VC investment (38%), followed by Financial Services (23%) and Exchanges (14%). Pure-play wallets are the smallest category at 1% of total VC investment.

It's not surprising to see that Bitcoin Payment Processors are receiving such a large share of venture funds. In a previous analysis we saw that processors, such as Visa and Mastercard, hold the largest market capitalizations (over $200 billion between the two companies) in traditional financial services sectors which Bitcoin could potentially disrupt.

It is interesting to note the relatively small VC investment in mining hardware companies (13%) given that it is very likely the largest legal revenue generating sector of the bitcoin economy with over $200m in mining hardware revenue to date.

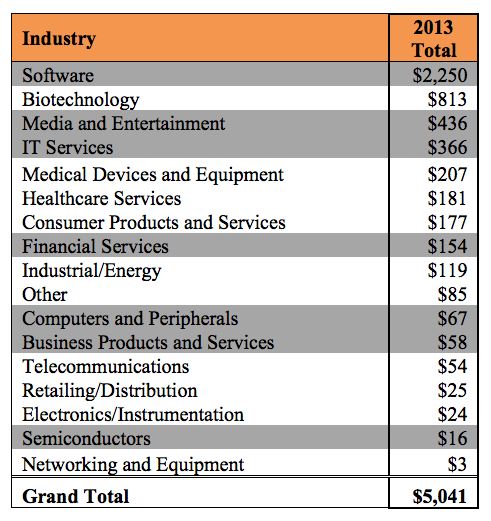

Table 4: VC Investments by Industry, 2013 ($m) for United States

vc-investments-industry-2013

While by no means insignificant, the $97.5m in publicly disclosed venture capital invested in bitcoin companies to date (Table 1) is relatively small compared with other investment sectors that have been beneficiaries of significant venture capital investment (Table 4).

The grey shaded areas of Table 4 are intended to highlight bitcoin-related investment sectors. For example, investments in bitcoin wallets could perhaps fall into more than one category, including Software and Financial Services.

Part two of this series, which will be published tomorrow, examines where the majority of VC investment in bitcoin companies has come from. Silicon Valley, surely? Not necessarily …

------------------------------------------------------------------------------------------------------

Notes on sources and methodology: unfortunately, the earliest industry-wide venture capital historical data is for 1995, two full years after the year Andreessen compares the Internet to bitcoin (1993). Bitcoin investment data spans 2012-early 2014 because the vast majority of bitcoin investments to date occurred in 2013. Please also note that no adjustment has been made for a number of other factors, such as inflation or changes in the cost of launching a startup over the past two decades.

DISCLOSURE

The leader in news and information on cryptocurrency, digital assets and the future of money, CoinDesk is a media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies. CoinDesk is an independent operating subsidiary of Digital Currency Group, which invests in cryptocurrencies and blockchain startups. As part of their compensation, certain CoinDesk employees, including editorial employees, may receive exposure to DCG equity in the form of stock appreciation rights, which vest over a multi-year period. CoinDesk journalists are not allowed to purchase stock outright in DCG.