2013 Bitcoin Trading Volume: The Winners and Losers

Recent reports that China-based exchange OkCoin may be fabricating data highlight the incentives for exchanges willing to inflate their reported trading volume.

The reason why an exchange might want to do this is quite simple: the bigger the volume an exchange appears to have, the more likely it is that liquidity-seeking traders will be attracted to that particular exchange.

Additionally, what makes inflating volume data even more tempting is that, unlike bitcoin price data, there is no independent method available to easily verify an exchange's reported volume data.

The prices which Bitcoin exchanges report can be verified by comparing actual trades at the quoted ask/bid with the prices that exchange is reporting through its API data stream (which most major exchanges now have). There should not be a significant discrepancy between two.

In contrast, given the anonymous nature of bitcoin transactions, and the lack of other market features such as a central clearinghouse, we are wholly reliant on each individual exchange for trading volume figures.

Is bitcoin trading volume data a fantasy?

While bitcoin exchanges have the motive and the means to readjust their volume figures, there are some good reasons why we shouldn't dismiss their data completely.

As Bitcoin matures, one can imagine a day when independent auditors will verify reported volume data, in the way that professional accounting firms certify the public financial statements for corporations.

In the meantime, the closest approximation we have to independent audits are the venture capital firms, which are investing in various bitcoin exchanges.

For example, Lightspeed Venture Partners recently made a $5m investment in BTC China. As a well respected venture firm, we can reasonably expect that Lightspeed audited BTC China's volume data as part of their due diligence process, particularly given how important this data is to the value of the investment.

Further, while there is some dispute over the recent OkCoin reports, the story does illustrates how some traders are watching the exchanges for possible discrepancies.

In the OkCoin example, it is also interesting to contrast Bitcoin customer activism with the lethargy of traditional bank customers, who take very little interest in the reporting and operations of their banks because deposits are insured.

In the wake of the 2008 financial crisis, some scholars, such as Paul Seabright of the University of Toulouse, have questioned whether the financial system would have been more secure had it been more like Bitcoin’s. In other words, Seabright conjectured that the financial system could be made more stable by having bank customers play a more active role alongside regulators in monitoring financial institutions by reducing/removing deposit insurance, thereby giving them more ‘skin in the game’.

The topsy-turvy world of bitcoin exchanges

With these caveats and disclaimers on volume out of the way, what can be said about trading volume for bitcoin this year, as we approach the end of 2013?

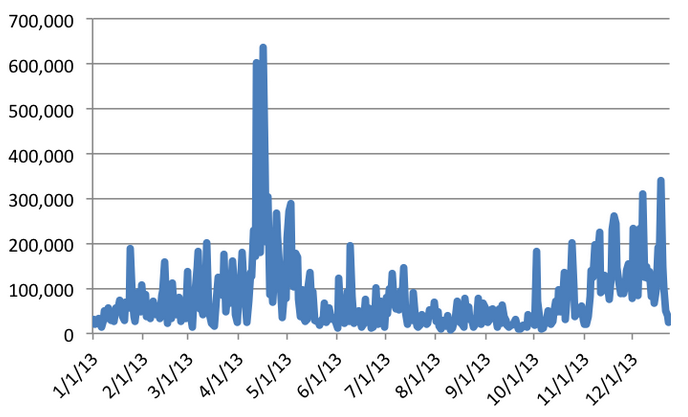

Figure 1: 2013 BTC Volume (units) – Cumulative Volume for BTC China, Mt. Gox and Bitstamp

CoinDesk.com, Bitcoincharts.com

One of the most striking elements of Figure 1 – which depicts the cumulative 2013 bitcoin trading volume across three leading exchanges – is that even with the dramatic upswing in November's prices, we have still not yet seen the same level of volume as mid-April.

The cumulative volume of 636,571 BTC on 16th April – the largest volume day of 2013 – is nearly double the peak November-December volume of 340,727 BTC on 18th December.

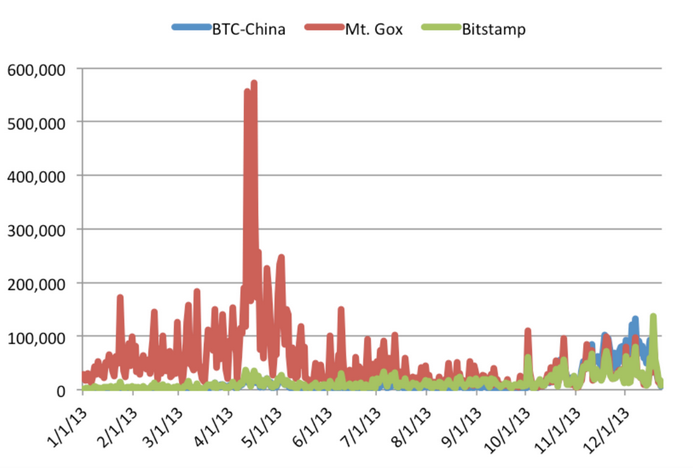

Figure 2: 2013 BTC Volume (units) – BTC China, Mt. Gox and Bitstamp

CoinDesk.com, Bitcoincharts.com

It is also worth noting the shift in the dispersion of volume between the April and November-December periods. As can be seen in Figure 2, Mt. Gox dominated bitcoin-trading volume through the first half of 2013, and beyond.

For example, on 16 April, the number of bitcoins traded on Mt. Gox alone equaled 572,186 BTC (90% of the total of the three exchanges).

In contrast, on 18 December there was a roughly equal dispersion across BTC China, Mt. Gox and Bitstamp, with a volume of 93,934, 109,723, and 137,070 BTC respectively.

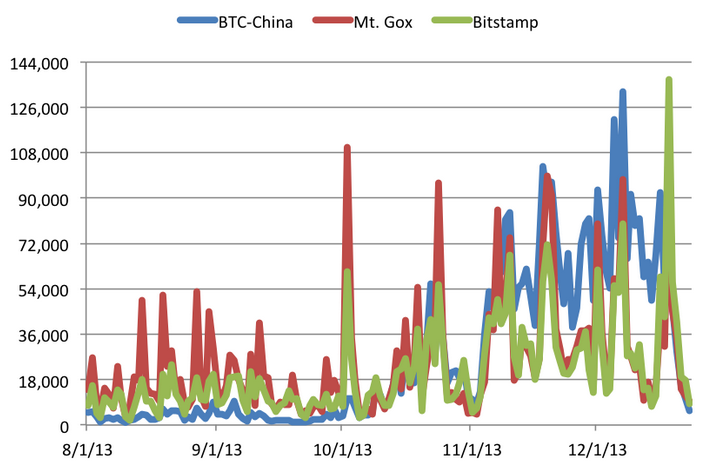

Figure 3: 1st August – 23rd December BTC Volume (units) – BTC China, Mt. Gox and Bitstamp

CoinDesk.com, Bitcoincharts.com

More recently, we can see in Figure 3 how BTC China has caught up to and overtaken Mt. Gox and Bitstamp in daily trading volume, again as measured by the number of bitcoins exchanged.

From 20 October through to 23 December, the average daily trading volume on BTC China has been 55,216 BTC, while Mt. Gox and Bitstamp have averaged exchanging 34,192 and 32,235 BTC per day, respectively.

However, if we look at most recent days we already see a dramatic reversal of fortune, with BTC China now falling behind both Mt. Gox and Bitstamp. In the last four trading days, BTC China’s average daily volume has been 15,293 BTC, whereas Mt. Gox and Bitstamp have averaged 17,434 and 21,574 BTC.

Why hasn’t bitcoin volume matched its April highs? Which exchanges are poised to pull ahead in 2014? Share your thoughts on these and other exchange volume issues in the comments below.

Race image via Shutterstock

DISCLOSURE

The leader in news and information on cryptocurrency, digital assets and the future of money, CoinDesk is a media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies. CoinDesk is an independent operating subsidiary of Digital Currency Group, which invests in cryptocurrencies and blockchain startups. As part of their compensation, certain CoinDesk employees, including editorial employees, may receive exposure to DCG equity in the form of stock appreciation rights, which vest over a multi-year period. CoinDesk journalists are not allowed to purchase stock outright in DCG.