Bitcoin, Ether Bounce After Disastrous Week for Crypto Market

The crypto market is going through a relief rally on Monday as bargain hunting is helping major coins regain some poise following last week's drubbing.

Bitcoin, the top cryptocurrency by market value, is changing hands near $36,500 at press time, representing a 5% gain on the day. The rise comes after a 25% decline over the week ended May 23 – the second straight weekly loss and the biggest since March 2020, per CoinDesk 20 data.

Ether, the second-largest cryptocurrency, is trading 8% higher at $2,257 (up 7.6%), having dropped by 41% over the same period – its most significant weekly decline on record.

Other prominent coins including Binance's BNB token, internet computer protocol (ICP) , bitcoin cash and polkadot are seeing 8% to 10% gains. Coins associated with decentralized finance (DeFi) such as LINK and UNI are trading 22% and 13% higher, respectively.

Demand from wealthy investors looks to have brought relief to the battered cryptocurrencies.

"Crypto funds, macro funds, opportunistic venture capitalists are beginning to buy this dip in BTC, ETH as well as blue-chip DeFi by staggering limit orders and running longer time-weighted average prices," crypto financial services provider Amber Group tweeted early Monday.

Bridgewater Associates founder Ray Dalio stated that he owns some bitcoin during an interview, recorded on May 6 and broadcasted Monday during Consensus by CoinDesk 2021.

“Personally, I’d rather have bitcoin than a bond” in an inflationary scenario, Dalio said during an hour-long conversation with CoinDesk Chief Content Officer Michael J. Casey.

The dip-buying shows large investors remain confident of long-term bullish prospects of cryptocurrencies in the wake of recent environmental and regulatory concerns. "The long-term thesis for crypto remains unchanged. Inflation, decentralization, privacy, programmability, seizure-resistance, and censorship-resistance …these are the secular drivers of adoption," angel investor and entrepreneur Balaji Srinivasan tweeted.

The market mood soured earlier this month after the U.S. electric car maker Tesla suspended vehicle purchases with bitcoin, citing high fossil-fuel use by miners. The surprise move dampened hopes for increased corporate adoption triggered by the company's decision to enlist bitcoin as a payments alternative in February.

Further, China, which supposedly accounts for most of the computing power dedicated to bitcoin's blockchain, reiterated its ban on cryptocurrency mining last week, drawing additional selling pressure for the cryptocurrency.

Bitcoin fell to a 3.5-month low of $30,000 last week, marking a 53% drop from the record high of $64,801 reached on April 14. Meanwhile, ether fell to below $2,000.

The downturn was largely the result of selling by "weak hands" and short-term traders. "From the end of April until now, wallet addresses holding bitcoin for less than one month dropped from 5.06 million addresses to 4.37 million, a loss of 690,000," the Defiant Newsletter said on May 18.

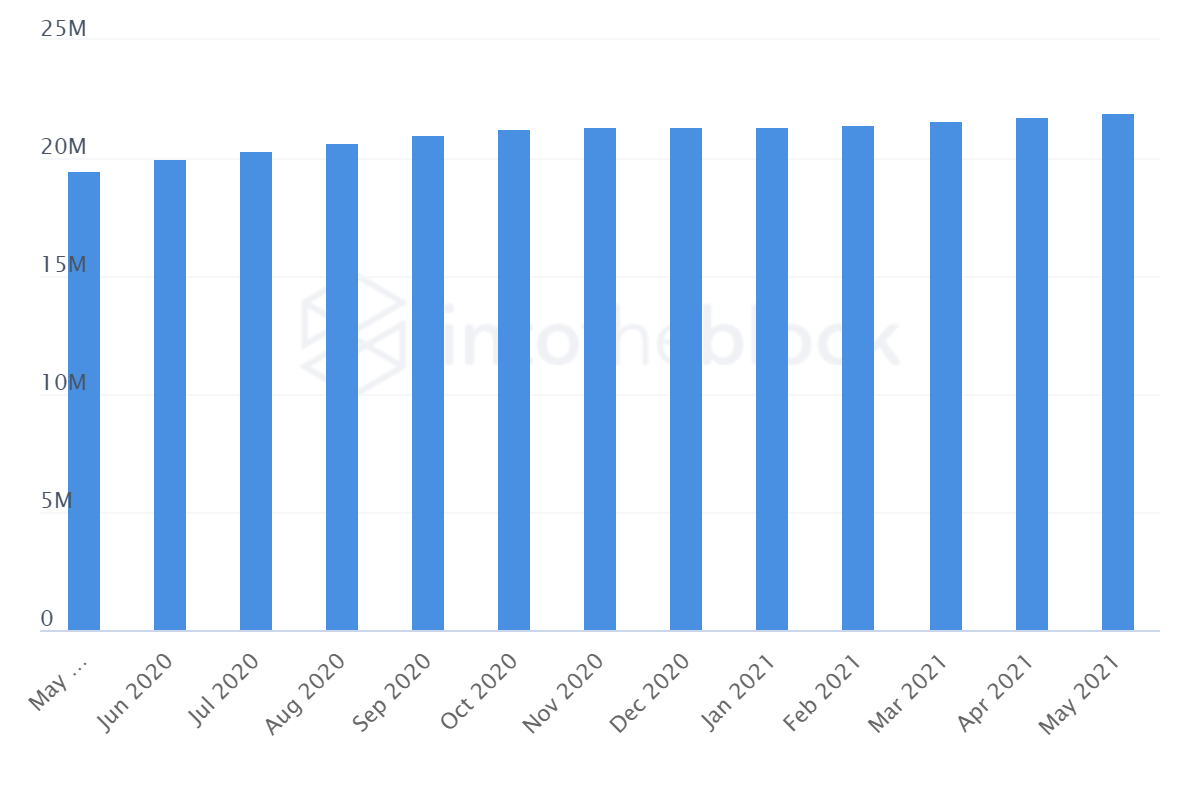

However, the number of addresses holding bitcoin for more than one year, dubbed as "holders" by IntoTheBlock, increased by 120,000 from 21.81 million to 21.93 million.

Bitcoin holders: Address holding coins for atleast a year

Moving ahead, a V-shaped recovery to $50,000 and higher may remain elusive, as the recent sell-off has shaken investor confidence. Moreover, according to some observers, the market may soon receive more negative news out of China. On Friday, a top Chinese governmental body called for a crackdown on cryptocurrency mining, amplifying regulatory concerns.

Some industry experts believe the negative news has been priced in, and the psychological support at $30,000 is likely to hold.

"Historically, such news from China (regarding mining and trading bans) have resulted in major drops for BTC, and this time is no different," Joe DiPasquale, CEO of BitBull Capital, said. "However, like the previous instances, BTC does recover, and the latest news isn't reflecting any new developments per se."

"Moving forward, $30,000 is a strong support and we can expect it to hold for now," DiPasquale added.

DISCLOSURE

The leader in news and information on cryptocurrency, digital assets and the future of money, CoinDesk is a media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies. CoinDesk is an independent operating subsidiary of Digital Currency Group, which invests in cryptocurrencies and blockchain startups. As part of their compensation, certain CoinDesk employees, including editorial employees, may receive exposure to DCG equity in the form of stock appreciation rights, which vest over a multi-year period. CoinDesk journalists are not allowed to purchase stock outright in DCG.