Circle Isn't Winning the Stablecoin Transparency Race

USD Coin is the second-largest stablecoin in the world. Tether, the largest stablecoin, has always been the more opaque product. But the transparency advantage enjoyed by USD Coin – issued by Circle Internet Financial – appears to be declining.

To comply with the terms of its settlement with the New York attorney general’s office, Tether is now providing the public with quarterly breakdowns of the investments used to back tether stablecoins. Tether has also started to issue periodic attestation reports that disclose the value of those investments, a practice USD Coin adopted several years ago.

Meanwhile, Circle is investing USD Coin customer funds in something it refers to as "approved investments." We have no clarity on what those investments are or how much Circle has allocated to them.

It's been over a year since Circle began to invest USD Coin funds in approved investments. Up until Feb. 28, 2020, just before the pandemic hit, Circle held all of its customer funds in accounts at federally insured U.S. banks. Products like checking accounts and time deposits would qualify. We know that from disclosures in Circle's February 2020 attestation report for USD Coin.

Regular attestation reports have become the industry standard for providing stablecoin consumers with transparency. An auditor verifies information about the investments that an issuer holds to back the stablecoins it has issued. The auditor's opinion is then published on the issuer’s website for public consumption.

In its subsequent attestation report, dated March 31, 2020, Circle added the category "approved investments." In short, Circle started to invest USD Coin customers' funds not only in accounts at federally insured U.S. banks, but also in a new type of financial asset.

At the time Circle made this change, the pandemic was shutting down the global economy. Short-term risk-free interest rates had collapsed from over 1.5% to nearly 0% in March 2020. Because Circle makes money from the interest it harvests by investing customer funds, its revenue would probably have been collapsing. To help compensate for the decline in short-term rates, it's a fair assumption that Circle was shifting USD Coin's investments into longer-term debt products that yield more. Longer-term securities tend to be riskier than short-term ones.

Unfortunately, Circle's attestation reports don't provide any information on the nature of its approved investments. So all we can do is guess at what those might be. Nor do we know what portion of its assets are held as approved investments – 99%? 1%?

The question of USD Coin's approved investments has only gotten more pressing as it has grown. Back in early 2020 when it first began to buy approved investments, Circle had issued only $400 million in USD Coins. But now there are about $25 billion USD Coins in circulation. That's a lot. It’s almost as big as PayPal.

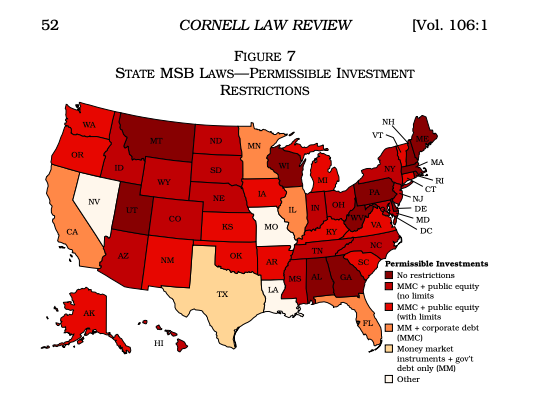

We have some clues into what those approved investments might be. Circle is a licensed money transmitter, having secured 44 state-issued money transmitter licenses. As a condition of granting licenses, state licensing boards typically limit the licensee's ability to invest customer funds to a list of "permissible investments."

For instance, a money transmitter with a Texas money transmitter license can only invest its customers' funds in very safe assets that include accounts or certificates of deposit, or both, at federally insured banks, government debt and money-market funds that invest in government debt.

That's a pretty confidence-inspiring list of investments. If you're a USD Coin owner and Circle is following the rules as set out by Texas law, you can breathe a sigh of relief. That means that Circle's approved investments are probably something relatively safe, say two-year Treasury notes. And thus your stash of USD Coins is well-secured.

New York and Connecticut have more lenient permissible investment restrictions. They allow money transmitters to invest in high-quality commercial paper, a type of short-term debt issued by corporations, as well as preferred shares of publicly listed companies.

So if Circle is following either New York or Connecticut regulations for investing a portion of its assets, its approved investments could consist of Nike preferred shares or Exxon Mobil commercial paper.

That's riskier, but not off the charts.

Things get a little more concerning under the rules of state licensing authorities in Alabama, Delaware, Georgia, New Hampshire, Pennsylvania, West Virginia and Wisconsin. Licensing boards in those states put no restrictions on what sorts of investments a licensee can invest in. (I am indebted to Dan Awrey's paper Bad Money for data on permissible investment rules.)

So if Circle is using Pennsylvania's money transmitter law as the basis for defining its approved investments, it could in theory own anything. Tesla shares? S&P 500 futures? Bitcoin? Tether?

Permissible investments for money services businesses, by state.

Now to be fair, I highly doubt Circle would choose to invest customer funds in risky assets. However, Circle doesn’t provide the public with any detail on which states’ permissible investments rules it is following. Without more disclosure on how to map state requirements over to USD Coin’s investments, it's impossible for outsiders to disprove such admittedly zany theories.

For someone who holds just $50 USD Coin, it’s probably not a big deal if Circle has shifted over to riskier investments. If those assets are impaired, that might mean a $1 or $2 loss on $50. But for someone who holds millions of dollars' worth of USD Coins (MakerDAO is currently the largest owner, at $3.2 billion USD Coins), then the nature of Circle’s approved investments becomes a very important question. These large and sophisticated holders need to do due diligence on their investments. Circle’s lack of transparency prevents that.

Responding to CoinDesk’s question about the nature of Circle’s approved investments, Circle told us the following: “USDC has become the world’s most trusted and well-regulated dollar digital currency in no small measure because of our adherence to strict reserve management and asset allocation policies. These are designed to exceed the demands of USDC in circulation with cash, cash equivalents and short-duration investment-grade assets consistent with our regulatory requirements and supervision under U.S. state banking laws.”

That sheds a bit more light on Circle’s approved investments, suggesting a combination of cash equivalents, perhaps commercial paper and money-market funds and short-duration investment grade assets. A step forward would be to provide additional details in its monthly attestation reports. That would mean disclosing each month what its approved investments are and how much it has allocated to them.

Also concerning is the steady slowing down in the publication of Circle's attestation reports, as first recounted by Andrew Rennhack. Last year, Circle would typically publish its USD Coin reports 15 days or so after the end of a month. Now reports are appearing on Circle’s website almost two months late. Circle's most recent USD Coin attestation report dates to April 30, more than two months ago.

I don't think anything nefarious is occurring. The problem is that two-month-old information isn't very valuable to stablecoin consumers.

Other stablecoin issuers offer quicker turnaround. Paxos and Gemini, for instance, have already published their May 28 reports. TrueUSD leads the pack with real-time 24/7 attestations. It should be possible for Circle to pick up the pace.

A Circle spokesperson suggests to CoinDesk that USD Coin’s fast growth makes that difficult: “The timeliness of issuing attestations have been impacted by the growth in demand for USDC, and its expansion on multiple blockchains, while remaining uncompromising about thoroughness of these reviews.”

Finally, Circle recently stopped disclosing the precise amount of U.S. dollars it holds in custody, as reported by Doomberg. Circle probably has good reasons for doing so, but why didn't it disclose those reasons in its USD Coin attestation report?

In sum, USD Coin's relative transparency advantage has been declining. With a few fixes, it has the chance to win first-pole position in stablecoin transparency.

I’d suggest that it’s in Circle's best interests to shoot for more transparency. Stablecoins don't pay interest to stablecoin consumers. That means that stablecoin consumers are not compensated for the risks incurred by the stablecoin issuer’s investment decisions. And so a consumer’s decision on what stablecoin to buy boils down to a very simple rule: Only hold the stablecoins that have the safest investment policies.

Put differently, in the long term the stablecoin game is a race to transparency. To the most forthcoming and prudent go the spoils.

DISCLOSURE

The leader in news and information on cryptocurrency, digital assets and the future of money, CoinDesk is a media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies. CoinDesk is an independent operating subsidiary of Digital Currency Group, which invests in cryptocurrencies and blockchain startups. As part of their compensation, certain CoinDesk employees, including editorial employees, may receive exposure to DCG equity in the form of stock appreciation rights, which vest over a multi-year period. CoinDesk journalists are not allowed to purchase stock outright in DCG.