Compounding and Saving in Bitcoin: The Power of a Dollar-Cost Averaging Strategy

Isaiah Douglass, CFP®, CEPA, is a partner at Vincere Wealth Management.

Frequently, I hear other advisors say, “I can’t buy bitcoin for clients; it’s too volatile and adds too much risk.” They’re also worried about purchasing power and inflation with savings rates at 0.50% or less. Bitcoin is an emerging asset class with a market cap of over $1 trillion. Bitcoin is often called a store of value, and its goal is to be better money. It achieves this by consensus rules and not allowing any single entity or group to change the monetary properties without the majority agreeing.

Before you question bitcoin’s store of value component, let’s look at the U.S. dollar. Consider that the dollar has lost 91% of its purchasing power since 1950, and the creation of dollars has accelerated dramatically since 2020. Now, let’s look at bitcoin as a savings tool and technology – particularly, through a strategy of dollar-cost averaging, the consistent purchasing of something over an extended period of time. You don’t go “all-in” in this strategy, but instead look to allocate an amount over a predetermined period of time. This period can have an end date or simply be until you decide to stop.

First, let’s say hypothetically that you had the worst luck with timing ever. You bought the absolute top of the first bitcoin cycle in 2011; if you held for 37 months, you did not lose money. (Rarely would I advocate for a large single lump-sum purchase hoping to find the “right” time to buy bitcoin.) If you understand scarcity and that there will never be more than 21 million bitcoin, when it comes to trying to time the perfect buy, this popular Chinese proverb rings true: “The best time to plant a tree was 20 years ago, and the second-best time is now.”

Bitcoin as a savings tool

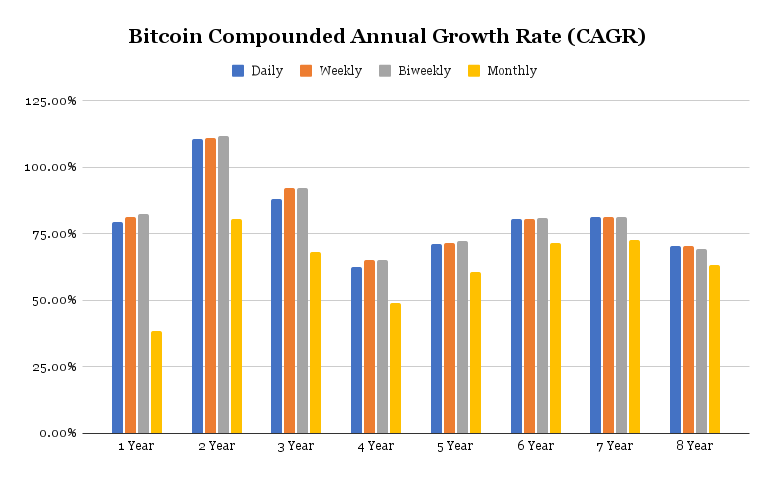

You will never be able to time the perfect entry in any initial purchase. The chart below shows the compound annual growth rate (CAGR) of bitcoin over various periods while buying at different intervals. Again, if you had the world’s worst timing and started dollar-cost averaging monthly right into the 2017 price run-up from under $1,000 to a peak of $20,000, you would have still compounded at over 48%.

Bitcoin CAGR as of 10/23/2021 (dcabtc.com)

Bitcoin is a savings technology and a store of value when you save consistently. As advisors, we advocate that clients automate savings all the time when planning for goals and retirement. Now you’re using a better method to help them save. You don’t need to turn off all the savings they are doing in other assets. An option here, for example, is to carve off a portion for bitcoin and allow the adoption rate of bitcoin, which is rivaling that of the internet in 1997, and network effects of better money work in your client’s favor. Thinking about volatility? Dollar-cost averaging reduces that impact.

Future growth

Looking toward the future, you might question the likelihood of these CAGRs. Let’s remember that bitcoin is a $1 trillion asset with limited retail, institutional and nation-state adoption. Bitcoin investment firm NYDIG estimated in January of this year that 10% of Americans owned bitcoin. (There was no mention of the dollar amount owned, which would lead one to believe the percentage with serious capital allocated to bitcoin is significantly lower.)

Notably, based on data on rolling four-year CAGRs for bitcoin, the absolute worst time frame was from April 9, 2013, to April 9, 2017, with a CAGR of 52%. The best CAGR was an eye-popping 235%, for the period from June 18, 2012, to June 18, 2016. The ten-year CAGR for bitcoin is 146%, even with large 80%-90% drawdowns.

When looking at the adoption curve, it’s hard to argue we are not still in the early innings for bitcoin. Recently the first bitcoin futures ETF was just launched, and the Houston Firefighters Pension Fund became the first public pension plan in the U.S. to invest in digital assets. As adoption accelerates, I fully expect that CAGRs will start to compress and decline.

Let’s assume that the following ten-year CAGR will be the worst dollar-cost averaging CAGR we’ve seen, which is 48%. That’s a 67% reduction from the previous ten-year CAGR of 146% – which is not an unrealistic expectation. Why, you might ask? Bitcoin is a fixed-supply asset – the only way to reflect demand is through the price.

Today, there are six publicly traded bitcoin mining companies all holding bitcoin they mine –that’s the only way for new bitcoin to be created – and raising inexpensive debt to allow them not to sell to finance operations. Business-intelligence software company MicroStrategy holds over 114,000 bitcoin. El Salvador has adopted a bitcoin standard. All of these developments did not happen in the last ten years, and retail ownership and demand is continuing to increase. The CAGR of Bitcoin may reduce, but demand is increasing and supply of liquid Bitcoin for sale is decreasing. (One easy way to track liquid supply is via Glassnode.)

Bitcoin dollar-cost averaging: an example

Here’s a scenario: What would it look like for someone to take a 2.5% allocation in bitcoin with a hypothetical $500,000 portfolio, then dollar-cost average at $280 per month? What impact does this have on wealth over time, and is the risk worth the reward?

Under this scenario, you’d have the client save $33,600 over the next ten years, and that initial $12,500 investment would grow to be $2,181,625. Is that risking too much of the portfolio at 2.5%? Is $3,360 per year asking too much to save for someone with a $500,000 portfolio? You could likely fund the bitcoin dollar-cost averaging strategy with the income from that traditional portfolio. In my opinion, this is highly doable for most clients, and provides an outcome all of the clients I’ve talked with would embrace.

And what if you instead stick to what we’ve seen work – the S&P 500? If you did the same thing, you’d end up at the end of the decade with $136,654. (That’s at a CAGR of 15.30%, one of the highest over the last 100 years.) This begs the question of whether that’s sustainable – and that should be questioned, as the S&P 500 is arguably overvalued. (One could look at the price to earnings, price to sales, U.S. market value divided by GDP, or CAPE Ratio, for instance.) It’s hard outside of an interest rate model to find a valuation metric on which the U.S. stock market is not flashing red. The opportunity cost to not allocate to bitcoin looks massive when compared to the U.S. stock market.

Saving in bitcoin moving forward

Your clients are looking to you for answers, including how they can maintain purchasing power with market uncertainty. You understand the merits of diversification and its impacts on portfolio construction; think of how your clients are saving as well. Consider starting a dollar-cost averaging strategy for your clients.

As the data shows, you don’t need to be perfect in selecting when to start, or whether you choose daily, weekly or monthly. The act of saving in bitcoin changes the impact those funds can have over time. The result might be that clients have the option to retire sooner – based on your saving recommendations.

DISCLOSURE

The leader in news and information on cryptocurrency, digital assets and the future of money, CoinDesk is a media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies. CoinDesk is an independent operating subsidiary of Digital Currency Group, which invests in cryptocurrencies and blockchain startups. As part of their compensation, certain CoinDesk employees, including editorial employees, may receive exposure to DCG equity in the form of stock appreciation rights, which vest over a multi-year period. CoinDesk journalists are not allowed to purchase stock outright in DCG.