Could Bitcoin Surpass Google's $384 Billion Market Cap?

Just how big a financial opportunity is Bitcoin?

Recently, Wall Street has been starting to ask that very question, paying more and more attention to the upstart alternative currency.

The first analysis by a registered broker dealer which attempted to value bitcoin's worth was published on 1 December by Wedbush Securities.

While Los Angeles-based Wedbush is a respected securities firm, it doesn't count itself among the first-tier of investment banks, or the ‘bulge bracket’ as its known on Wall Street. The Wedbush research report contained some novel analysis and perspective, but it was also ‘light’ in that it weighed in at just one and a half pages.

In short, it was not yet clear just how interested Wall Street was in Bitcoin.

However, when bulge bracket member Bank of America Merrill Lynch (BAML) and its well-regarded currency analyst David Woo followed Wedbush’s lead with a detailed 11-page report and valuation analysis, it became clear that Wall Street was taking the cryptocurrency seriously.

Bitcoin’s price is only part of what interests Wall Street

What grabbed the most headlines from both the Wedbush and BAML research reports was the bitcoin price analysis offered by the competing houses.

[post-quote]

David Woo and his team at BAML gave a maximum fair value estimate for Bitcoin of $1,300. Gil Luria and Aaron Turner of Webush shied away from providing a specific number, instead suggesting a potential 10x-100x range above its value at the time of their report.

What grabbed fewer headlines, but was arguably more interesting, were the comments in each report about the real opportunity Bitcoin presents to disrupt the existing financial services industry.

In the words of Luria and Turner: “the long-term threat posed by this technology is mostly to the payment networks (V, MA) and technology facilitators such as CIW, in our opinion. We believe [cryptocurrency] technology may have advantages in introducing new capabilities and a superior point-to-point cost structure to the current hub-and-spoke branded networks.”

The natural follow-on question from this is just how big are the payment networks and technology facilitators?

Measuring Bitcoin’s disruption potential

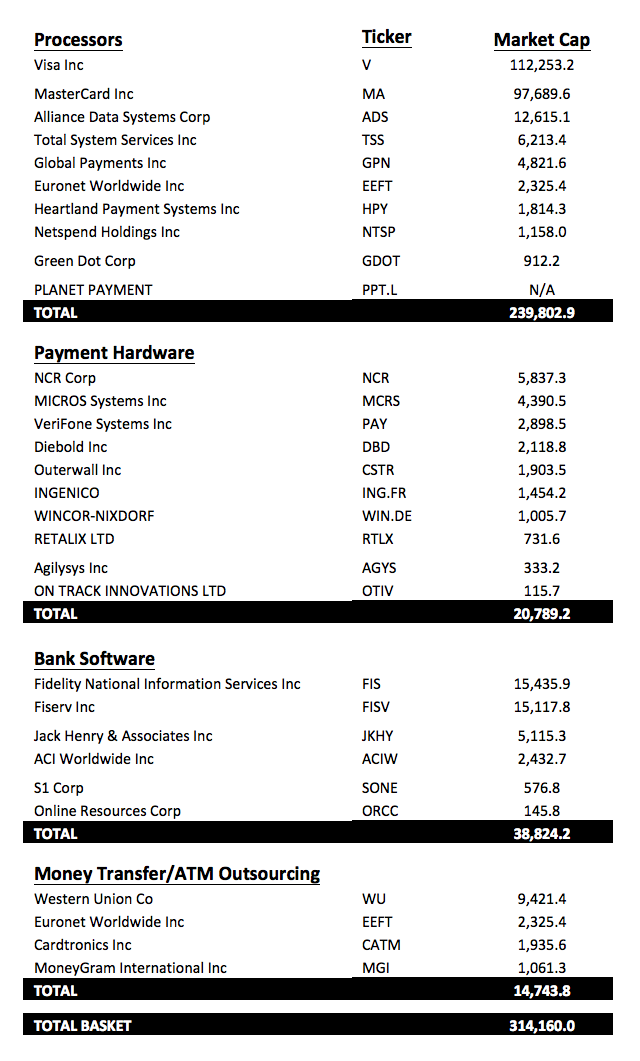

Table 1 below presents a list of companies in four sectors which Bitcoin and its surrounding ecosystem touch – payment processors, payment hardware, bank software, and money transfer and ATM outsourcing.

Table 1: Bitcoin Ecosystem - Comparable Company Market Caps ($s millions)

Sources: Data as of January 10, 2014. CoinDesk, Wedbush Securities

The first point worth highlighting is that the combined total market capitalization for the basket of companies in Table 1 was $314bn as of 10th January, 2014. This is a significant figure, and not so far off from the current market capitalization of Google ($384bn).

In short, if you were simply wondering why venture capitalists are interested in investing in Bitcoin then you need not look any further than this number.

(Note: An important feature to observe about the basket of companies presented above is that it is largely dominated by North American firms. While many of the above companies are global leaders, the basket is missing European and Asian firms due to data availability constraints. This analysis may thus materially skew downwards the total global market capitalization for these sectors of the financial services industry.)

Of the $314bn in total market cap, it is also interesting to note that $210bn in market cap (or two-thirds of the total for this basket of companies) is made up by just two firms: Visa and Mastercard. The value which is concentrated in these two payment processors speaks volumes about why venture capitalists have focused their largest investments to date in bitcoin processors such as Coinbase.

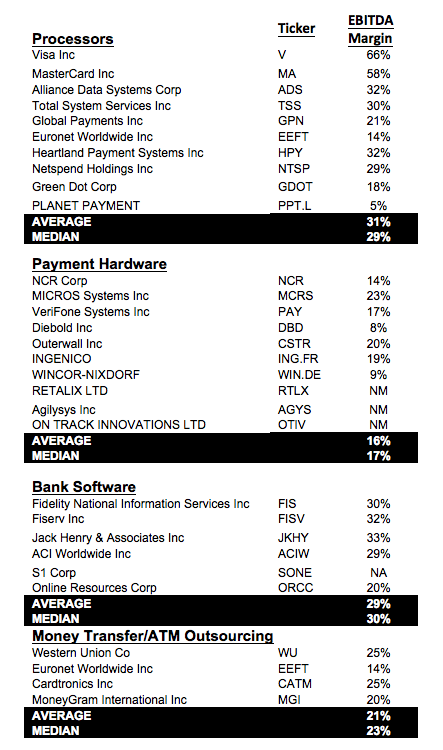

Large Market Caps = Large Profit Margins

Why do some of the companies in Table 1 have much larger market caps than others?

Factors such as total revenue, growth opportunity and management team (among other elements) all play an important role in determining valuation for publicly traded companies. But the single financial measure which Wall Street arguably obsesses over more than any other is profit margins.

Table 2: Bitcoin Ecosystem - Comparable Company EBITDA Margins

Sources: Data as of January 10, 2014. CoinDesk, Wedbush Securities

Table 2 summarizes the EBITDA margins for the same basket of companies. Here we can quickly see part of story behind why Visa and Mastercard have such large market capitalizations. The two payment processors have the highest EBITDA margins in the basket at 66% and 58%, respectively. Such high margins make for an attractive target for would be disrupters.

While it is tempting to focus on the largest companies which Bitcoin has the opportunity to disrupt, smaller operators should also fear Bitcoin.

The largest of the money transfer and ATM outsourcing companies, Western Union, has a $9bn market cap, which is not far from Twitter’s market cap at its IPO pricing. Part of the reason for Western Union’s high market cap is that the firm can earn upwards of 10% per transaction on international remittances, leading to a plump EBITDA margins of 25%.

The overall size of the sectors which Bitcoin has the potential to disrupt combined with relatively fat profit margins explain a significant reason behind why investors and Wall Street see big things in store for Bitcoin.

Opportunity Image via Shutterstock

DISCLOSURE

The leader in news and information on cryptocurrency, digital assets and the future of money, CoinDesk is a media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies. CoinDesk is an independent operating subsidiary of Digital Currency Group, which invests in cryptocurrencies and blockchain startups. As part of their compensation, certain CoinDesk employees, including editorial employees, may receive exposure to DCG equity in the form of stock appreciation rights, which vest over a multi-year period. CoinDesk journalists are not allowed to purchase stock outright in DCG.