Dogecoin and the New Meaning of Money

In an ugly week for markets, it’s striking the crypto news that caught even more attention in the mainstream media was not bitcoin’s whopping 24% drop from its peak early Saturday morning, but dogecoin’s spectacular rally earlier in the week. This week’s column dives into why that phenomenon, while literally built on a joke concept, is not something to be laughed at. The surprising clout of the DOGE mob speaks volumes about how power is being redrawn in the digital age.

And for this week’s podcast episode, we deliberately turn a blind eye to the number-go-up (and down) obsessions of the crypto market and talk about what really matters: human dignity. Sheila Warren and I talk to Human Rights Foundation Chief Strategy Officer Alex Gladstein and a Sudanese activist who uses the pseudonym Mo and the handle @SudanHODL for his podcast to talk about what bitcoin, as a “global neutral money,” can do for human rights.

Have a listen after reading the newsletter.

The Doge age

A part of me worried I was giving in to temptation by writing this column.

There’s an understandable concern within the CoinDesk newsroom that covering dogecoin could signal that we favor easy clicks from fanatics over the risk of encouraging bubble-fueled investments in a coin with no inherent technical advantages.

But then I read Max Read’s excellent piece on the future of money from last week, which inspired a delightful New York Magazine cover that asked the question, “Can I SPAC my Stonks With NFTs?” I now realize – hear me out – there’s no more important story about the reimagination of money right now than $DOGE’s crazy price surge. (See the chart in the next section.)

Dogecoin mania, as exemplified by the cryptocurrency community’s failed quest this week to get its price above 69 cents on Tuesday in honor of a 04/20/69 date meme associated with “national stoner day,” doesn’t just seem frivolous, it is. Yet, there’s real, serious money at stake.

In that sense, dogecoin’s wild ride encapsulates an important moment in human history. Society’s traditional “story” of money is breaking down, where new, head-scratching concepts like SPACs (special purpose acquisition companies) and NFTs (non-fungible tokens) are flourishing, and where fun and games and mob-buying can overwhelm markets.

Doge is part of an intense competition for meaning within the world of money, a testament to the 21st century power shifts fueled by two separate financial crises and by the rise of social media networks. Let’s explore them.

The story’s end

We start with the idea that money is a story.

Regular readers will know I’m a fan of Yuval Harari, whose bestselling “Sapiens” argued that human civilization is built on our capacity to organize around commonly believed imagined concepts.

Harari’s examples of these constructed ideas included “the corporation” and “the nation-state,” among others that have enabled us to form complex societies. It’s money, though, he says, that’s “the most successful story ever told.”

Currencies do not have a core, intrinsic value. (Sorry, gold bugs, that applies to your favorite shiny metal as much to paper money and cryptocurrencies.) A currency’s value is dependent on shared belief in that value. That’s not to say certain types of money don't have qualities that help its story resonate, which is why bitcoin can be described as “sound money” and dogecoin cannot. But without belief, all money is worthless.

For much of the past two millennia, the dominant story was that money’s value flowed from the sovereign because the state, empowered with taxation, had an overarching interest in optimizing the societal accounting function that is money’s true purpose. Then, more recently, in the era of fiat money it was the “good faith and credit” of the government (rather than a fixed supply of gold) that would guarantee that value. Later, that story was enhanced by the idea politically independent central banks would maintain a currency’s value by managing its supply in society’s best interest.

Now, as we enter into a phase where state-backed money competes with both decentralized cryptographic money such as bitcoin or dogecoin and with corporate money such as diem (formerly libra) or Starbucks points, that narrowly defined story is falling apart. The first catalyst came a little more than a decade ago.

Crisis moment

In his piece, Read traces the current breakdown to an interview then-Federal Reserve Chairman Ben Bernanke gave to "60 Minutes” in 2009 at the height of the financial crisis. Asked if the Fed’s monetary injections into troubled banks were funded by taxpayers, Bernanke shook his head and said: “To lend to a bank, we simply use the computer to mark up the size of the account that they have with the Fed.”

He was telling it as it had long been: The Fed creates money by adding to or reducing banks’ reserves. But to the confused masses grappling with financial meltdown it was a revelatory challenge to the foundational story.

It revealed that the creation of money is not bound by some sacred rule of scarcity and is mostly unrelated to the coins and banknotes that stand, in our collective imagination, as its representative units of value. It showed money as a digital accounting system a single entity can adjust through a few clicks on a computer.

Fast forward to March 2020 and a new crisis: COVID-19. Amid a tanking global economy and a desperate scramble for dollars, the Fed took its “quantitative easing” policy into overdrive, declaring it will put as many fresh computer-based dollars as needed onto banks’ balance sheets to stave off financial collapse, with no upper limit on the program. It also expanded the category of assets it accepts in return for those new dollars to include corporate debt, exchange traded funds and other non-government instruments. It now seems the Fed will buy almost anything to prop up markets.

Meanwhile, the “trillions” numbers attached to stimulus efforts in this new era of “QE infinity” are so unfathomably big that, as Bloomberg columnist Jared Dillian noted last spring, “money is losing its meaning.

This erosion of meaning is leading people to question money’s value, which is naturally leading them to buy other things. It is reflected in the surging prices for assets that seem to outsiders to be unhinged from real-world value: in bitcoin, in Gamestop stock, in NFTs and, yes, in dogecoin.

But before we get to Doge, consider another contributing factor: social media.

Leaderless online communities

Social media has challenged the central organizing structure of pre-internet society. Although the internet has failed to address wealth inequality in aggregate, the power for anyone to publish, and to do so pseudonymously, has had a democratizing effect, empowering communities to generate new stories around which to organize.

This is meme culture. Social media enables the crowdsourcing of stories around memes, which in turn generates new forms of belief, a sense of purpose and camaraderie. And with that, these communities can, for once, stand up to the established order.

That’s what we saw in the GameStop phenomenon, where a 7 million-strong Reddit community drove up the price of its favorite game retailer’s stock to impose huge losses on hedge funds that had tried to short-sell it on the view that its value was out of touch with reality.

The dogecoin phenomenon is similar, with a key difference: There is no focal point for a regulator or a powerful Wall Street money manager to exert pressure against. This is a big departure from the GameStop case, where regulators and private equity funds essentially combined forces to stop Robinhood, the WallStreetBets group’s favored trading app, from processing trades in the stock, causing its price to collapse.

With dogecoin, not only is there no one in charge of the cryptocurrency, trading activity is spread across dozens of exchanges, some of which are themselves decentralized.

Who or what would a regulator go after? Dogecoin was created – as a joke, literally – by someone who not only quit the project but the entire crypto movement. Like Bitcoin, there was no premine or initial coin offering creating pre-launch tokens for founders and there is still no identifiable team of leaders able to manipulate dogecoin’s performance to its benefit and at the expense of others.

Marketing meets memes

For now at least, this structure leaves the far-flung, fanatical Doge community to go about its collective business of meme and buzz creation, stirring speculation in the coin.

Equally important, it’s creating unique opportunities for others to hitch their wagon to this quirky, community-powered brand and its prevailing Shina Ibu logo: an image of fun, of absurdist irony and of common interest – a brand fit for the Gen-Z and millennial-led internet age. This is, in turn, giving rise to a new, symbiotic model for marketing as brands look to leverage the Doge community’s high-value engagement.

A defining moment came with Slim Jim’s imaginative Doge-driven social media marketing campaign. But the foundation was laid in the early days of the dogecoin community, recounted recently by CoinDesk’s Ollie Leach, when enthusiasts spontaneously contributed to various marketing campaigns to boost the coin’s prominence. In 2014, there was a dogecoin-sponsored Nascar driver and, in a stroke of genius, the dogecoin-funded Jamaican bobsleigh team.

Dogecoin will never be what bitcoin is or aspires to be: a store of value, a global reserve currency and a future medium of exchange for a decentralized economy. But in this unique convergence of memes, a fun brand, a strong community formation and some powerful marketing clout, we see how the 21st century digital media economy is reconceptualizing money.

This does not mean you should invest in dogecoin. It does mean the Doge phenomenon matters.

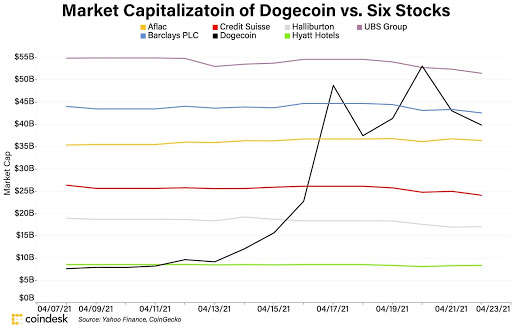

Off the charts: Doge and the goliaths

Today’s chart tracks dogecoin’s wild price ride against the performance of some well-established corporate names on Wall Street.

Just two weeks ago, dogecoin’s market cap was $8.3 billion, just below that of Hyatt Hotels. Then it started rising, not only beating out the hotel chain but also surpassing, in quick succession, the valuations of engineering giant Halliburton, banking conglomerate Credit Suisse and insurer Aflac. Then, last weekend, the $DOGE market cap rose above $45 billion to get beyond that of 330-year-old British bank Barclays, before peaking on Monday at $53.98 billion, a hair above Swiss banking giant UBS.

Since then, dogecoin’s valuation has slipped back and was just below $40 billion on Thursday afternoon. That’s on par with asset management giant T. Rowe Price.

Not bad for a joke coin.

Sign up to receive Money Reimagined in your inbox, every Friday.

The Conversation: Bitcoin Vs Gold

Stansberry Research staged a much-anticipated debate this week between MicroStrategy CEO Michael Saylor, who is a prominent bitcoin advocate, and investor Frank Giustra, a fan of gold and a bitcoin skeptic. It got a lot of attention.

Saylor, who crowdsourced his debate prep with the help of a sci-fi themed battle scene, opened with some big statements. He suggested that if a deity were to come down and design the perfect “God coin” system, Bitcoin would come closest to having the same attributes. (For the record, he also provided a detailed description of how Bitcoin works and why he believes it is the highest form of “sound money.”)

The imagery and hyperbole seemed to irk Giustra, who said the use of laser eyes and other crypto-insider jokes made Bitcoin “feel like a cult.” In a follow-up tweet, gold market media outlet Gold Telegraph chose to emphasize that point by superimposing alongside a video of Giustra an image of a laser-eyed Saylor as the Pied Piper, leading a crowd to its demise.

Who won? Predictably, opinions divided along tribal lines, though bitcoiners seemed more confident of Saylor’s victory than gold bugs were of Giustra’s. Here’s podcaster and prominent bitcoin supporter Preston Pysh, whose Twitter feed was full of snippets of the MicoStrategy CEO making “devastating” points against his opponent.

In contrast, outspoken gold investor and bitcoin critic James Rickards declared that “Frank won on substance” in what was the “best ever” gold vs. bitcoin debate.

Relevant Reads: Regulation Rumors

The weeklong bitcoin price rout began last weekend in rather dubious fashion.

- As Omkar Godbole reported, bitcoin plunged $8,000 early Sunday to a three-week low of $52,148. This happened after the Twitter account FXHedge, which mostly posts all-cap headlines from mainstream news reports, published a since-removed tweet saying the U.S. Treasury was about to charge financial institutions over crypto-based money laundering.

- The veracity of that report was questionable. As Nikhilesh De explained on CoinDesk TV’s "First Mover", it appeared somewhat related to reports Friday that new Securities and Exchange Commission Chairman Gary Gensler was awaiting a report from Treasury Secretary Janet Yellen on the cryptocurrency industry before moving forward with his agency’s own blueprint for the sector. But Nik’s sources gave every impression that the story of an impending crackdown was unfounded.

- Maybe the truth wasn’t what mattered. As Kevin Reynolds pointed out in a well-timed opinion piece later that day, the perfect recipe for a crypto sell-off had been prepared: the market had soared and new rookie investors were nervous. So when the FXHedge report combined with a CNBC tweet of a month-old story about Indian banning crypto and erroneous accounts that Coinbase CEO Brian Armstrong had sold most of this stock (when in fact he’d only sold 1.5%), the market was primed to go lower.

- Still, once that downturn had happened, bitcoin was unable to recover and on Thursday underwent another big downturn, this time doing so in sync with wider financial markets, which got whacked by reports the Biden Administration is planning to drastically increase capital gains tax rates. At the time of print, the leading cryptocurrency was poised to clock its worst week since mid-February. And as Brad Keoun reports, it “dominance” ratio had tellingly dropped below 50% of total crypto market cap as ether and other altcoins were relatively less harmed by the declines.

DISCLOSURE

The leader in news and information on cryptocurrency, digital assets and the future of money, CoinDesk is a media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies. CoinDesk is an independent operating subsidiary of Digital Currency Group, which invests in cryptocurrencies and blockchain startups. As part of their compensation, certain CoinDesk employees, including editorial employees, may receive exposure to DCG equity in the form of stock appreciation rights, which vest over a multi-year period. CoinDesk journalists are not allowed to purchase stock outright in DCG.