Dying for a Bitcoin Futures ETF? Watch Out for ‘Contango Bleed’

Improved prospects of the U.S. approving a futures-based bitcoin (BTC) exchange-traded fund (ETF) has brought cheer to the crypto market.

However, the fund may fail to match bitcoin’s price performance thanks to a scary-sounding market dynamic known as “contango bleed.” This refers to fund underperformance that could theoretically occur because longer-dated futures contracts are trading at higher prices than shorter-dated contracts.

In commodities markets, it’s considered normal for prices on longer-dated contracts to trade above those on shorter-dated contracts; this is known as “contango.” The price spread often roughly correlates with the cost of storage – such as for oil or soybeans. There’s also the time value of money: the foregone yield that an investor might get from socking money into interest-bearing securities like U.S. Treasury bonds. In the bitcoin market, contango mainly results from bullish price expectations.

Such contango could prove a liability, though, if the U.S. Securities and Exchange Commission approves a bitcoin-futures ETF. Several futures ETF proposals are due for regulatory approval in the coming weeks, of which the ProShares’ product is widely expected to receive accreditation on Oct. 18. Investors who pile into these new funds could get hit with “contango bleed,” where they might get lower returns than if they had simply bought bitcoin directly.

The dynamic shows one potential downside from the SEC’s preference for an ETF based on bitcoin futures over one that buys bitcoin directly. While Gensler has suggested that a futures-based ETF might be less risky for investors because it’s rooted in regulatory commodity markets – bitcoin futures are traded on the Chicago-based CME exchange – the “contango bleed” might represent a consistent source of underperformance.

“The futures-based ETF, if approved, will be an inefficient product,” Ilan Solot, global market strategist at Brown Brothers Harriman, told CoinDesk. “Because bitcoin’s futures curve is typically in contango, the fund is going to suffer from a negative rollover.”

“I am expecting the average negative yield to be at around 5%-10% on the CME bitcoin futures curve,” said Patrick Heusser, head of trading at Swiss-based Crypto Finance AG. In plain English, if the price of bitcoin doubles in the next 12 months, the ETF would underperform by at least 5%-10%.

Futures-based ETFs allow investors to gain exposure to the underlying asset via a futures contract – an obligation to buy or sell the underlying at a later date at an agreed-upon price. The contracts expire once a month so the rollover is needed for investors to maintain the exposure.

However, the process often results in a loss because on the expiry day the contract due for settlement tends to converge with the spot price, while the out-month contracts still trade at a premium. Investors might end up selling the contract due for expiry at a loss and buying the next one at a high price.

Unhedged investors would still benefit from any underlying gains in bitcoin’s price – just not as much, because of the contango bleed.

“If the futures curve is in contango and the serial months are all premium to the preceding, you are bleeding the difference between the months every month,” said one trader for a major crypto exchange, who asked not to be named because of employer-imposed restrictions on making public statements.

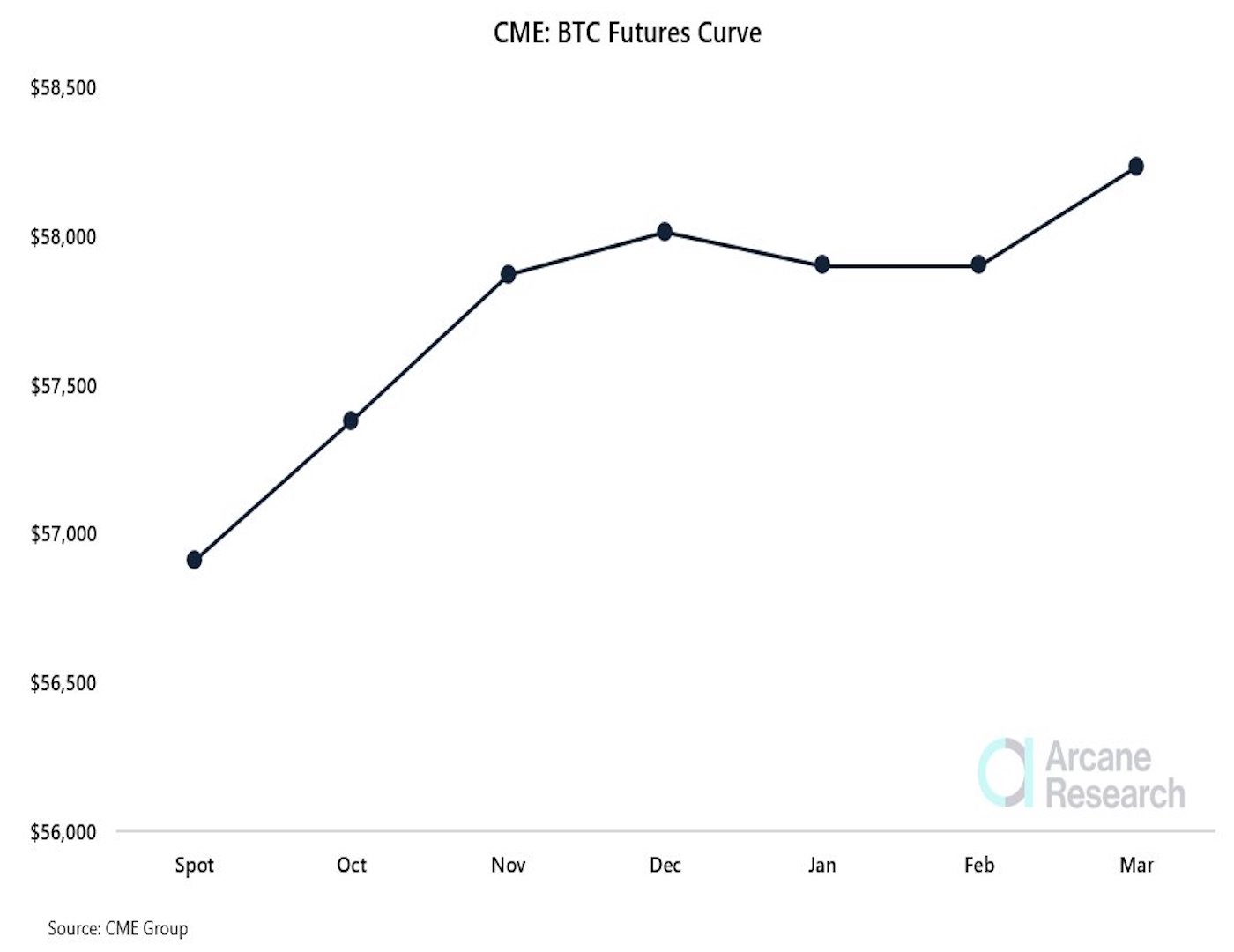

The CME data shows bitcoin’s October expiry contract is currently trading at $58,000, for a premium of roughly $500 over the spot price, while the November expiry is changing hands at $58,500, or a premium around $1,000.

Assume a newly approved bitcoin futures ETF purchases the October contract at the current price.

By month’s end the premium in the October contract would likely evaporate. So when the fund resets its exposure, it could end up selling the October contract at a loss of $500 or 0.86% (annualized 10.34%) and then having to buy the subsequent month’s contract at a premium.

The ProShares Bitcoin Strategy ETF, widely expected to receive approval on Oct. 18, mentions the rollover risk in its prospectus as a key risk for investors: “Extended periods of contango could cause significant losses for the fund.”

“We’ve seen this phenomenon in commodities and other futures markets for years,” Trey Griggs, CEO at crypto trading firm GSR, told CoinDesk in a Telegram chat. “When the forward curve is in contango, particularly steep contango, long-only ETF and ETN [exchange-traded note] investors get nickel-and-dimed each month by having to pay the roll.”

“Often, the price investors pay for the roll exceeds the absolute return of the underlying, causing the investment to earn negative yield even in a rising price environment,” Triggs added. In such cases, the fund tends to lose value over time, as evidenced by the futures ETF tied to Chicago Board Options Exchange’s volatility index (VIX).

“The $VXX is a VIX ETF and suffers from strong contango bleed,” trader and analyst Alex Kruger tweeted. “This is how its long-term chart looks like. Yes, it looks like death. You never go long $VXX unless for a short period of time.”

“The roll period is different for every asset,” one trader from a crypto exchange said. “Historically, the roll period on the CME has usually occurred in the last week before contract expiration.”

Negative roll not seen as a big deterrent

According to experts, the prospect of a futures ETF underperforming bitcoin is unlikely to deter investors from pouring money into the product.

“Investors simply want exposure to the asset class and will look the other way if there is a slight roll charge,” GSR’s Griggs said. “In our view, the only way the roll charge will prevent investor interest in a BTC ETF is for the forward market to be in very steep contango, far steeper than we’ve previously seen in BTC futures.”

If contango steepens, fund managers could change strategy and hold more than just the front-month futures contract.

ProShares’ ETF proposal says: “The Advisor will utilize active management techniques to seek to mitigate the negative impact or, in certain cases, benefit from the contango or backwardation present in the various futures contract markets, but there can be no guarantee that it will be successful in doing so.” Backwardation is the opposite of contango.

DISCLOSURE

The leader in news and information on cryptocurrency, digital assets and the future of money, CoinDesk is a media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies. CoinDesk is an independent operating subsidiary of Digital Currency Group, which invests in cryptocurrencies and blockchain startups. As part of their compensation, certain CoinDesk employees, including editorial employees, may receive exposure to DCG equity in the form of stock appreciation rights, which vest over a multi-year period. CoinDesk journalists are not allowed to purchase stock outright in DCG.

Omkar Godbole is the senior reporter on CoinDesk's Markets team.