Move Over, Carry Trade, These Retail-Friendly DeFi Options Strategies Yield 12%-30%

The crypto “cash-and-carry” trade – where traders simultaneously enter into a long position on bitcoin or ether (ETH) in the spot market and then a short position in the futures market, a way of betting on eventual convergence of the two prices – has lost its shine.

Reliable for 30% annualized gains earlier this year, the opportunity has since shrunk to single digits, as the frenzied bullishness witnessed in cryptocurrency markets earlier this year faded and as major exchanges reined in leverage.

But investors can still make double-digit returns via weekly ether or bitcoin “covered call” strategies offered by decentralized finance (DeFi) asset management platforms, including Ribbon Finance and StakeDAO. And it’s a heck of a lot easier; all you have to do is deposit coins in “strategy vaults” designed to automate the trade.

A popular traditional market strategy, “covered calls” involve selling out-of-the-money (OTM) call options, or those with strike prices above the current market level, while owning the underlying asset. It is typically seen as a neutral to bullish strategy, because the upside is capped. A call option gives the holder the right but not the obligation to buy the underlying asset at a predetermined price on or before a specific date. A call option buyer is implicitly bullish, while the seller anticipates a price drop or consolidation and receives a premium for offering insurance to the purchaser.

Check that versus the cash-and-carry trades executed on Binance, the world’s largest centralized crypto exchange by volume: Traders would earn just 5%.

Just automate

With Stake DAO and Ribbon Finance, the strategy is automated. Users deposit their coins, wrapped ETH (wETH) or wrapped BTC (wBTC), into the strategy vaults, which take care of the complexities, like selecting the appropriate strike price for selling the weekly option.

These structured products open doors for the retail crowd to participate and earn yield from the otherwise complex options market, dominated mainly by sophisticated traders and institutions with ample capital and experience.

Where there’s the potential for outsize gains, there’s always risk. In addition to the market risks, DeFi protocols are prone to glitches and are sometimes targeted by sophisticated crypto-savvy attackers on the prowl for loopholes in the underlying code or flaws in the design.

But the emergence of this new category of offerings in the crypto options marketplace provides yet another example of how blockchain-industry developers are engineering cryptocurrency projects to replicate the structured-finance alchemy pioneered by Wall Street, and in some cases taking it to the next level.

“Options or derivatives can be pretty intimidating for retail traders,” Wade Prospere, head of marketing and community at decentralized options marketplace Opyn, told CoinDesk. ”Structured products such as Ribbon Finance and Stake DAO abstract away all the complexities involved in options trading like determining the strike price.” Both Ribbon Finance and Stake DAO use Opyn’s infrastructure to mint and trade the option tokens on-chain.

Launched in April, Ribbon Finance owns 95% of the DeFi asset management market, and its vaults are 30 times larger than those of Stake DAO. On Sept. 14, Ribbon finance announced the launch of its first two Ribbon V2 Vaults – the ETH Covered Call vault and the WBTC Covered Call Vault. For now, both V1 and V2 vaults are running concurrently.

While Ribbon’s staff plays the role of a vault manager and selects the strike price for the options, in V2 the process of selecting strikes is fully autonomous.

Meanwhile, Stake DAO manually selects the strikes at which options are sold, consistently targeting 10% delta options, which correspond to a strike price generally 25% above the current price. Early Thursday, Stake DAO launched DeFi’s first-ever open arbitrage strategy on the Avalanche platform.

Dissecting the strategy

Every Friday at 11:00 coordinated universal time (7 a.m. ET), Ribbon Finance’s vault keeps 10% of user funds aside and deposits 90% as collateral at Opyn to mint weekly European ETH call options. The vault receives Opyn’s oTokens, representing the ETH call options, and selects the strike price or the level at which calls are to be sold. One option contract is for 1 ETH.

The vault then sells these ETH calls over DeFi peer-to-peer marketplace Airswap in return for the options premium (paid in ether) by buyers, mostly market makers. The premium received represents the yield from the strategy and is distributed to users in proportion to their deposits.

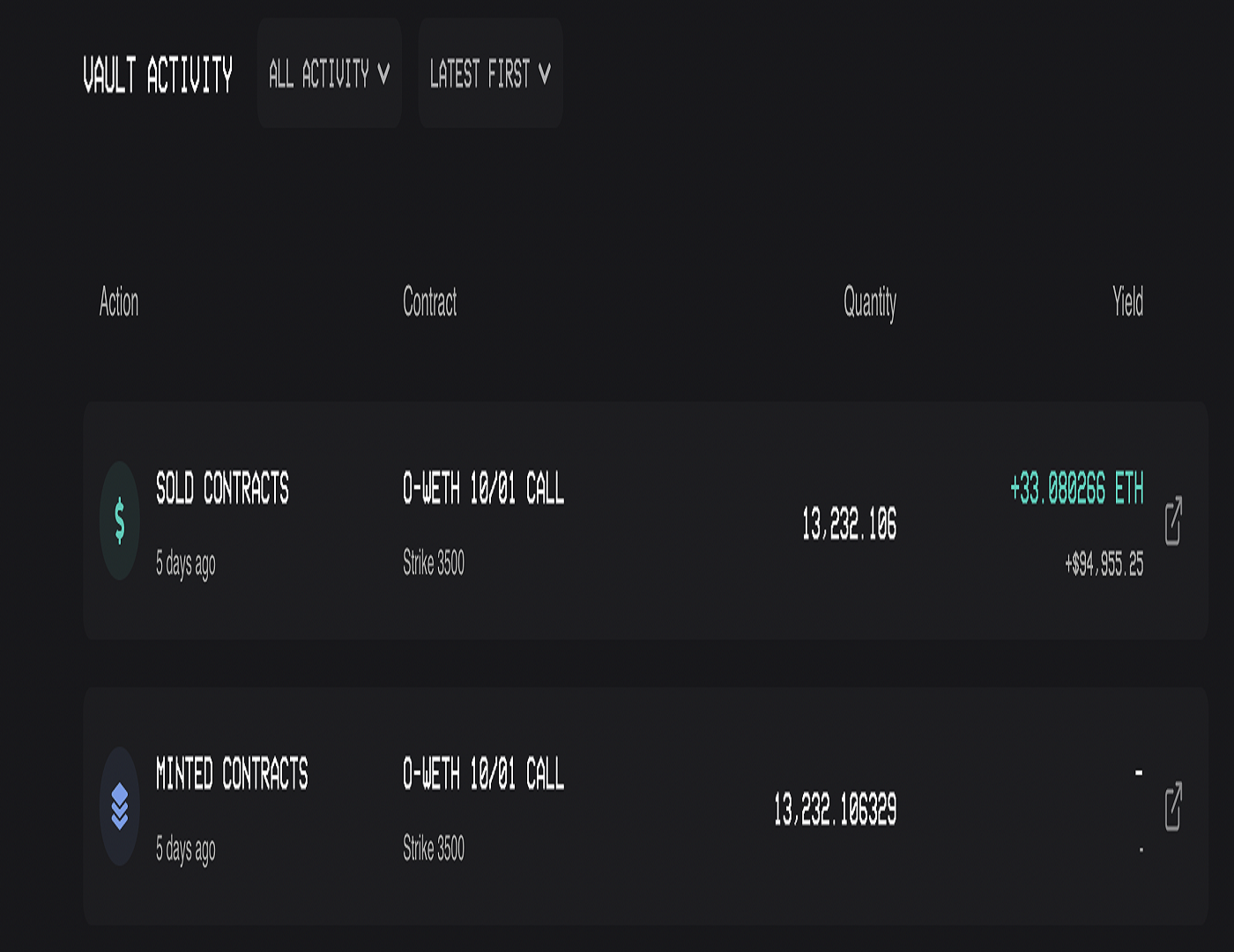

(Ribbon Finance)

Last Friday, Ribbon Finance minted and sold 13.2 million contracts of ether 3,500 strike call options expiring on Oct. 1. The vault received more than 33 ETH worth $94,955 in premium.

If ether remains below $3,500 on Friday, the options will expire worthless, and user deposits held as collateral at Opyn will be transferred back to users via Ribbon’s vault.

Risk profile

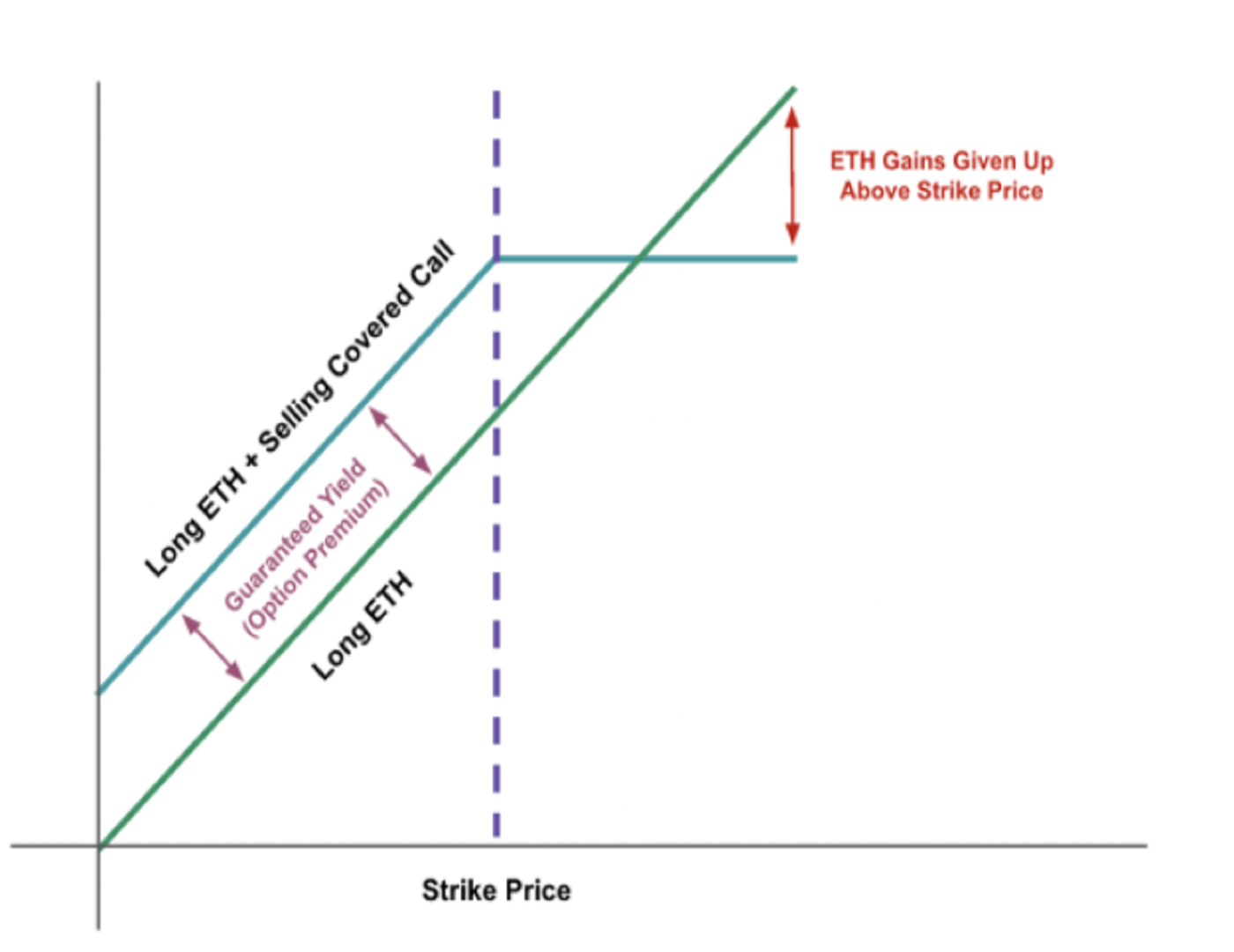

If the options expire in-the-money, say with ether settling at $3,600, options buyers (holders of oTokens) can exercise their options by withdrawing ETH from the Opyn vault. The amount withdrawn is equal to the difference between the strike price and the market price of ETH on the expiration date.

The options are cash-settled, and so for each option contract, buyers can withdraw $100 per contract in ETH from the vault ($3,600 minus $3,500). Any leftover ETH will be returned to the depositors.

(Opyn)

The chart above shows that vault depositors keep the yield from options premiums even when the options expire in the money, but the loss incurred is taken from the ETH collateral deposited. In other words, vault depositors lose the upside in ether once the cryptocurrency moves above the strike price at which calls have been sold.

Ribbon’s other products – the USDC-collateralized ETH put selling strategy and the WBTC covered call strategy – operate along similar lines.

Stake DAO’s ETH and BTC covered call strategies beef up returns by putting collateral (user deposits) to work in automated market maker Curve’s eCRV or sETH-ETH pool. The liquidity provider (LP) tokens received from Curve are then used as collateral to mint options at Opyn.

“We place those LP tokens from Curve inside the ETH covered call cycle,” Julien Bouteloup, founder of Stake DAO and Stake Capital, said. “That way, users earn yield from being liquidity provider at Curve in addition to premium received from selling call options.”

Both Stake DAO’s and Ribbon Finance’s vaults reinvest the yield earned from selling call options back into the strategy, compounding returns for depositors over time.

Why DeFi options

ETH or BTC holders can book a covered call strategy on a centralized exchange like Deribit by depositing their holdings and selling OTM calls.

In this case, the onus of determining the right strike price (the level at which the option is sold) lies with the trader. The job is easier said than done as traders need to assess historical volatility and expected volatility to come up with a strike price high enough so that with reasonable price movements, the option expires worthless. At the same time, it should be close enough to the market price to allow maximum inflow of premium. Higher strike calls trade relatively cheap versus lower strike calls.

With Stake DAO and Ribbon Finance, users get to bypass the hassle of studying market conditions and determining the apt strike price. As the Bankless newsletter wrote in an explanatory piece on Aug. 3, “two transactions and voilá, you’re in and earning automated returns in complex DeFi strategies.”

“The goal is to build a decentralized exchange that anyone can use and don’t necessarily need to understand the difficult concepts,” Bouteloup told CoinDesk. Bouteloup added that with centralized exchanges, users don’t have the option of boosting yields by putting collateral to work as Stake DAO does.

The DeFi structured products provide investors an opportunity to express various market views with tailor-made products.

Julian Koh, co-founder of Ribbon Finance, said the vaults help users by spreading out gas costs and making the strategy affordable to everyone. Gas refers to the fee required to successfully conduct a transaction or execute a contract on Ethereum’s blockchain. It tends to spike when the network faces congestion as it did following the recent Time magazine NFT launch. One address paid $70,000 for 10 of Time’s non-fungible tokens.

Such astronomical fees make it impossible for small investors to access DeFi protocols. Vaults alleviate this problem by distributing the gas costs across all depositors.

“Instead of doing three to four transactions per week per user, the vault will do three to four transactions per week for thousands of users at once,” Ribbon Finance’s official blog said. “This makes the user experience of using these Option Vaults extremely straightforward and relatively cheap – deposit, wait for yields and withdraw.”

Ribbon Finance’s ETH covered call vault has a maximum deposit capacity of 25,000 ETH, while StakeDAO’s strategy vault has an upper limit of 750 ETH.

“Vault limits have been introduced to make sure things don’t get too big too quickly,” Ribbon Finance’s Koh said. “We want to test the system cautiously.”

The future looks bright for the sub-sector, particularly with centralized avenues like Binance drawing regulatory ire. “As the fixed income and derivatives markets for crypto continue to mature, we will no doubt continue to see exciting developments in the structured products space from Ribbon Finance and other DeFi protocols continuing into the future,” Messari’s Alexander Beasant noted.

DISCLOSURE

The leader in news and information on cryptocurrency, digital assets and the future of money, CoinDesk is a media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies. CoinDesk is an independent operating subsidiary of Digital Currency Group, which invests in cryptocurrencies and blockchain startups. As part of their compensation, certain CoinDesk employees, including editorial employees, may receive exposure to DCG equity in the form of stock appreciation rights, which vest over a multi-year period. CoinDesk journalists are not allowed to purchase stock outright in DCG.

Omkar Godbole is the senior reporter on CoinDesk's Markets team.