Why Lower Bitcoin Price Volatility is No Panacea

Prior to the nearly 20% pullback in bitcoin’s price we’ve witnessed in the last 24-hours, there had been a fair amount of digital ink spilled suggesting that bitcoin’s price volatility may be decreasing.

Rob Wile of Business Insider, Alex Wilhelm of TechCrunch, and Timothy B. Lee of the venerable Washington Post all wrote pieces over the last week suggesting that bitcoin is becoming less volatile.

Before addressing the question of whether bitcoin volatility is in fact declining, why is bitcoin volatility important?

There are in fact several reasons, but all the recent articles explicitly or implicitly emphasize one view in particular, which is that bitcoin adoption should increase if the price becomes less volatile. For example, Alex Wilhelm of TechCrunch says:

I will come back to Wilhelm’s point at the end of this post, but first let’s examine the claim that bitcoin volatility is in decline.

Eyeballing bitcoin volatility

It does not take a PhD in statistics to make a few observations about bitcoin’s price volatility.

: Bitcoin Price, 3rd September 2013 – 29th January 2014.

The above Chart 1 is from Rob Wile’s post and is used to support the claim that bitcoin volatility has recently declined. The period that Rob highlights with a red arrow (the month of January 2014) certainly looks very flat and stable.

The CoinDesk Bitcoin Price Index (BPI) from 7th January through 4th February more-or-less agrees with Wile's data from Bitcoin Average, with the BPI range-bound between $800-$900 for the past month. [Editors note: this has since changed following today’s pullback.]

When our eyes deceive us

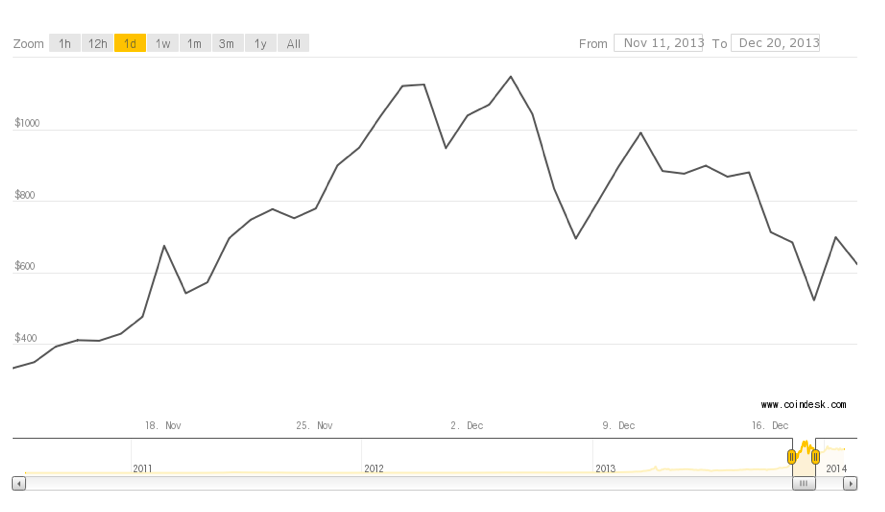

Now, comparing the recent period depicted in Wile’s Chart 1 with the immediately preceding period (11th November – 20th December) depicted below in Chart 2, it’s fair to say that our eyes aren’t misleading us.

, 11th November 2013 – 20th December 2014

In the month of November bitcoin’s price more than doubled, only to fall by over 50% in December following news that China had banned its banks from dealing in bitcoin. This price action is reflected visually in the jagged, 'mountain range' appearance of Chart 2.

In short, even with today’s pullback the last several weeks have seen nothing like the larger price swings and higher volatility seen back in November and December.

But here’s the question: have there not already been much longer periods of relative price stability following a large spike and then decline in bitcoin’s price than what has been observed since the beginning of January 2014?

In other words, even prior to today, were Wile et al getting a little ahead of things by intimating that the bitcoin volatility dragon has been slain?

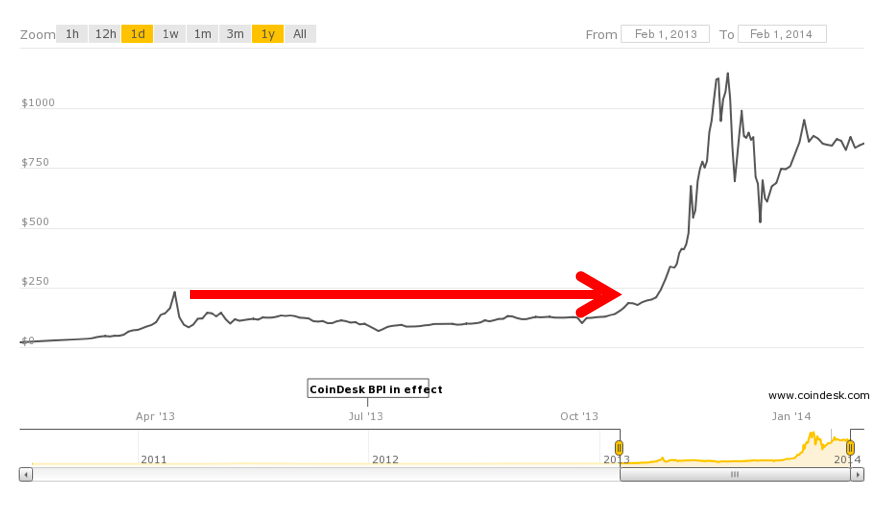

Chart 3 below depicts data taken from the CoinDesk Bitcoin Price Index over the past twelve months.

: CoinDesk Bitcoin Price Index, 4th February 2013 – 4th February 2014

For the six-month period following the April price collapse (May to October 2013, highlighted with the red arrow line) the price of bitcoin looks very flat, appearing to be about as stable as Wile’s Chart 1 depiction of January 2014 – but for a much longer period (six months vs Wile’s one month).

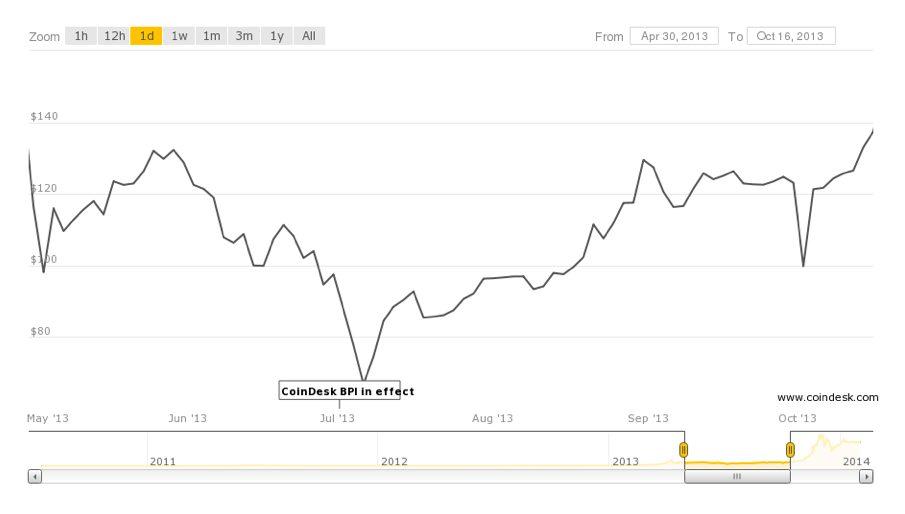

But zooming in on the red arrow period in Chart 3, we can see that our eyes are deceiving us.

: CoinDesk Bitcoin Price Index, 20th April 2013 – 16th October 2014

Chart 4 above reveals upon closer inspection that the period between late-April through mid-October was anything but ‘flat’.

For example, bitcoin’s price declined by approximately 50% on Mt. Gox from the June peak to the July trough. This 50% loss in value may not have been as dramatic as December’s sudden plunge, but it equals it in terms of percentage decline in bitcoin’s market cap.

Data visualization tricks of the trade

The above discussion and charts are intended to raise two points. The first being that the way data is visualized can have a significant impact on the conclusions we are likely draw from eyeballing charts used to make claims about, say, bitcoin volatility.

Why? Well, because adjustments to both the scale shown on the Y axis (vertical) and time period depicted by changing the X axis (horizontal) can significantly alter what the data appears to ‘say’ in charts.

For example, below, Wile’s chart (left) is positioned alongside a chart of the CoinDesk BPI (right) for the period of 7th January – 4th February 2014.

Here you can see how the period of time which appears flat in Wile’s chart on the left becomes a jagged mountain range when shown with different Y and X axis ranges on the BPI chart on the right. Wile accomplishes this by including earlier period data back through September, which allows for a larger scale Y axis.

This potential for the same data to tell a different story based on how it is visualized is not something Wile et al mention when making their claims.

This brings me to the second point, which is more of a question on whether statistical measures can provide a more robust means of explaining whether bitcoin volatility is decreasing.

Statistically speaking, is bitcoin’s price volatility declining?

The recent discussion of bitcoin volatility trends appears to have been kicked-off by a blog post on 20th January from Eli Dourado, a PhD student at George Mason and research fellow at the Mercatus Center.

Dourado’s blog post, which was titled ‘Bitcoin Volatility is Down Over the Last Three Years. Here’s the Chart that Proves It’, shows bitcoin’s historical volatility using price data from Mt. Gox.

Immediately we can see one potential problem with Dourado’s approach: his choice for source data. By relying solely on data from one exchange, Mt. Gox Eli brings into his analysis price elements which may only be related to issues at Mt. Gox.

These issues include downtime due to DDOS attacks, as well as the so-called ‘Mt. Gox Premium’ where bitcoin can often trade for as much as 20% more on Gox than other exchanges like Bitstamp or BTC-e which are part of the CoinDesk BPI. Dourado fails to acknowledge this problem.

His results, depicted in the chart below, show a declining trend in volatility, and that the trend is statistically significant with a univariate OLS regression yielding a t-score on the date variable of 15.

Putting aside the data source issue, does Dourado’s argument close the case and prove that bitcoin volatility is declining? Unfortunately the answer is not so simple.

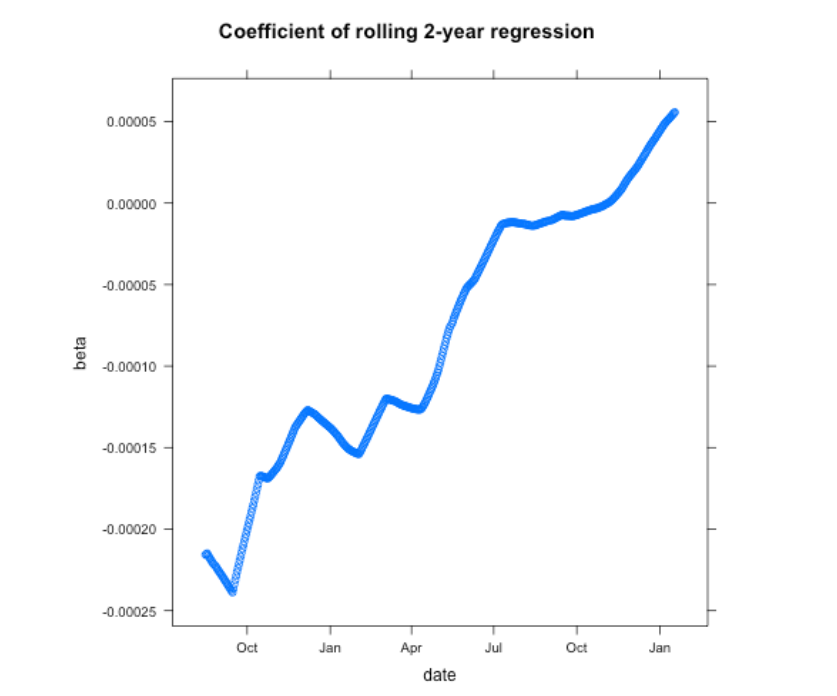

In response to Dourado’s post, Robert Sams over at Cryptonomics basically says “not so fast, Eli”, stating that Dourado’s “claim that 'there is a clear trend of falling volatility over time' isn’t defensible at all”.

In the chart below, Sams analyzes the same data, but instead of using Dourado’s 30-day rolling window method he employs a rolling two-year window. This, in effect, causes the early months of bitcoin to fall out of the sample period.

Source: Robert Sams, Cryptonomics

As Sams notes, his analysis “tells a very different story” than Dourado’s.

Matthew Martin, on his blog Separating Hyperplanes, also takes Dourado to task on his statistical method, and largely concurs with Sams’ critique. After performing several additional tests Martin concludes by saying: “I cannot tell you which way bitcoin volatility is going, but I can tell you that Dourado can't either.”

However, Dourado responded to Sams and Martin in the comments section of his original blog post and, while acknowledging their criticism, basically stands by the headline conclusion from his original analysis.

So where do things stand in the debate about trends in bitcoin volatility?

The bottom line here is that statistical methods can, in fact, face similar issues as data visualization when it comes to settling questions about bitcoin’s volatility. Sources, time periods chosen, methods, and other test design decisions often make statistical results less than definitive.

Put simply, where you place the statistical goalposts matters.

In terms of alternative volatility measures, as previously discussed, there are a number of reasons why calculating bitcoin’s beta coefficient (or ‘beta), a common measure for measuring volatility of securities, would appear to offer dubious value.

What’s missing from the recent bitcoin volatility debate

While there may be evidence to support both sides of the debate over bitcoin volatility trends, there is another important aspect of bitcoin volatility which is being overlooked.

Timothy B Lee of the Washington Post states that he sees a pattern in bitcoin’s price action, comparing this recent bounce back and stabilization with earlier bitcoin price action episodes. He concludes by stating that “bitcoin will stabilize in the future”.

And perhaps bitcoin will in fact stabilize in the ‘future’, whenever that may be. But what Lee and everyone else is failing to address is whether, from a pro-bitcoin perspective, lower bitcoin price volatility is desirable?

There is a view in the bitcoin community, captured in the earlier Wilhelm quote that “essentially the more wild the swings in its value, the less useful bitcoin is as a tool of commerce”, which is not entirely true.

Certainly, if you are interested in seeing more people holding bitcoins then, yes, one could argue that lower volatility could make it more attractive to hold bitcoins from day-to-day in the same way people hold US dollar banknotes in their wallets. Reduced volatility should build confidence in bitcoin as a stable store of value.

Lower bitcoin volatility is no panacea

However, the flip side of lower volatility is that bitcoin will lose many of the well-heeled momentum investors who are attracted to bitcoin’s relatively high volatility vis-à-vis other asset classes. And while it might be tempting to believe that bitcoin would be better off without these momentum traders, the bitcoin community needs to be careful what it wishes for here.

Today, bitcoin has a relatively small total market capitalization of around $9bn. A lower total market capitalization also equals less total potential liquidity, and liquidity is an extremely important driver in markets today.

One of the reasons investors are so attracted to the US Treasury bond market, for example, is because that at approximately $11tn in total publicly traded debt it is the deepest, most liquid asset market in the world today.

The Treasury market features a very large number of active buyers and sellers, allowing global investors to quickly move very large sums of money in and out of the US Treasuries.

In contrast, bitcoin’s relatively miniscule market capitalization and correspondingly thin liquidity make it a non-starter for many. One thing that would help change this is if bitcoin’s market cap increases.

A growing bitcoin market cap could have several positive knock-on effects, such as new businesses deciding to accept bitcoin, and institutional investors including bitcoin in their longer-term portfolio holdings.

Momentum investors could help further boost bitcoin’s market cap and overall liquidity during the current growth phase. However, if volatility vanishes then don’t expect these fast-moving traders to stick around.

Pill image via Shutterstock

DISCLOSURE

The leader in news and information on cryptocurrency, digital assets and the future of money, CoinDesk is a media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies. CoinDesk is an independent operating subsidiary of Digital Currency Group, which invests in cryptocurrencies and blockchain startups. As part of their compensation, certain CoinDesk employees, including editorial employees, may receive exposure to DCG equity in the form of stock appreciation rights, which vest over a multi-year period. CoinDesk journalists are not allowed to purchase stock outright in DCG.